AGENCY:

Federal Housing Finance Agency; Office of Federal Housing Enterprise Oversight.

ACTION:

Notice of proposed rulemaking; request for comments.

SUMMARY:

The Federal Housing Finance Agency (FHFA or the Agency) is seeking comments on a new regulatory capital framework for the Federal National Mortgage Association (Fannie Mae) and the Federal Home Loan Mortgage Corporation (Freddie Mac, and with Fannie Mae, each an Enterprise). The proposed rule would also make conforming amendments to definitions in FHFA's regulations for assessments and minimum capital and would also remove the Office of Federal Housing Enterprise Oversight's (OFHEO) regulation on capital for the Enterprises.

DATES:

Comments must be received on or before August 31, 2020.

ADDRESSES:

You may submit your comments on the proposed rule, identified by regulatory information number (RIN) 2590-AA95, by any one of the following methods:

- Agency Website: www.fhfa.gov/open-for-comment-or-input.

- Federal eRulemaking Portal: http://www.regulations.gov. Follow the instructions for submitting comments. If you submit your comment to the Federal eRulemaking Portal, please also send it by email to FHFA at RegComments@fhfa.gov to ensure timely receipt by FHFA. Include the following information in the subject line of your submission: Comments/RIN 2590-AA95.

- Hand Delivered/Courier: The hand delivery address is: Alfred M. Pollard, General Counsel, Attention: Comments/RIN 2590-AA95, Federal Housing Finance Agency, Eighth Floor, 400 Seventh Street SW, Washington, DC 20219. Deliver the package at the Seventh Street entrance Guard Desk, First Floor, on business days between 9 a.m. and 5 p.m.

- U.S. Mail, United Parcel Service, Federal Express, or Other Mail Service: The mailing address for comments is: Alfred M. Pollard, General Counsel, Attention: Comments/RIN 2590-AA95, Federal Housing Finance Agency, Eighth Floor, 400 Seventh Street SW, Washington, DC 20219. Please note that all mail sent to FHFA via U.S. Mail is routed through a national irradiation facility, a process that may delay delivery by approximately two weeks. For any time-sensitive correspondence, please plan accordingly.

FOR FURTHER INFORMATION CONTACT:

Naa Awaa Tagoe, Senior Associate Director, Office of Financial Analysis, Modeling & Simulations, (202) 649-3140, NaaAwaa.Tagoe@fhfa.gov; Andrew Varrieur, Associate Director, Office of Financial Analysis, Modeling & Simulations, (202) 649-3141, Andrew.Varrieur@fhfa.gov; or Miriam Smolen, Associate General Counsel, Office of General Counsel, (202) 649-3182, Miriam.Smolen@fhfa.gov. These are not toll-free numbers. The telephone number for the Telecommunications Device for the Deaf is (800) 877-8339.

SUPPLEMENTARY INFORMATION:

Comments

FHFA invites comments on all aspects of the proposed rule and will take all comments into consideration before issuing a final rule. Copies of all comments will be posted without change, and will include any personal information you provide such as your name, address, email address, and telephone number, on the FHFA website at http://www.fhfa.gov. In addition, copies of all comments received will be available for examination by the public through the electronic rulemaking docket for this proposed rule also located on the FHFA website.

Table of Contents

I. Introduction

II. Overview of the Proposed Rule

A. Regulatory Capital Requirements

B. Capital Buffers

C. Key Enhancements

D. Sizing of Regulatory Capital Expectations

1. Aggregate Regulatory Capital

2. 2018 Proposal's Capital Requirements

3. 2008 Financial Crisis Loss Experience

III. Background

A. Pre-Crisis Regulatory Capital Framework

B. Lessons of the 2008 Financial Crisis

1. Capital Adequacy

2. Going-Concern Standard

3. High-Quality Capital

4. Stability of the National Housing Finance Markets

C. Post-Crisis Changes to Regulatory Capital Frameworks

IV. Rationale for Re-Proposal

A. Responsibly Ending the Conservatorships

B. Ensuring Capital Adequacy

1. Quality of Capital

2. Quantity of Capital

C. Addressing Pro-Cyclicality

V. Definitions of Regulatory Capital

A. Statutory Definitions

B. Supplemental Definitions

1. Loss-Absorbing Capacity

2. Components of Regulatory Capital

3. Regulatory Adjustments and Deductions

VI. Capital Requirements

A. Risk-Based Capital Requirements

1. Supplemental Requirements

2. Risk-Weighted Assets

B. Leverage Ratio Requirements

1. Adjusted Total Assets

2. Tier 1 Leverage Ratio Requirement

3. Sizing of the Requirements

C. Enforcement

VII. Capital Buffers

A. Prescribed Capital Conservation Buffer Amount (PCCBA)

1. Stress Capital Buffer

2. Countercyclical Capital Buffer

3. Stability Capital Buffer

B. Leverage Buffer

C. Payout Restrictions

VIII. Credit Risk Capital: Standardized Approach

A. Single-Family Mortgage Exposures

1. Single-Family Business Models

2. Calibration Framework

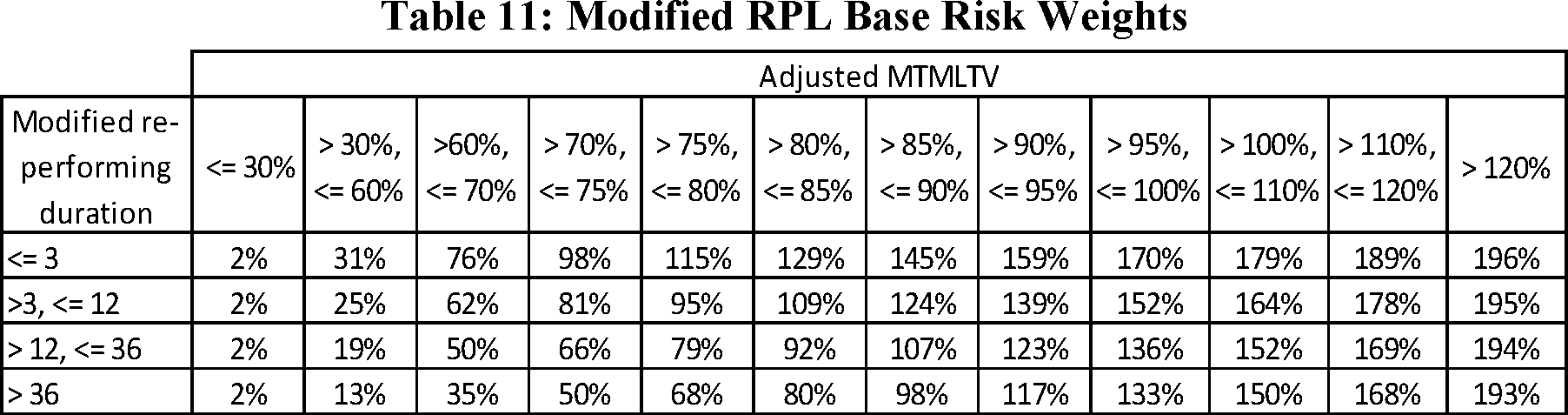

3. Base Risk Weights

4. Countercyclical Adjustment

5. Risk Multipliers

6. Credit Enhancement Multipliers

7. Minimum Adjusted Risk Weight

B. Multifamily Mortgage Exposures

1. Multifamily Business Models

2. Calibration Framework

3. Base Risk Weights

4. Countercyclical Adjustment

5. Risk Multipliers

6. Minimum Adjusted Risk Weight

C. CRT and Other Securitization Exposures

1. Background

2. PLS and Other Non-CRT Securitization Exposures

3. Retained CRT Exposures

D. Other Exposures

1. Commitments and Other Off-Balance Sheet Exposures

2. Exposures to Sovereigns

3. Crossholdings of Enterprise MBS

4. Corporate Exposures

5. OTC Derivative Contracts

6. Cleared Transactions

7. Credit Risk Mitigation

IX. Credit Risk Capital: Advanced Approach

X. Market Risk Capital

A. Standardized Approach

1. Single Point Approach

2. Spread Duration Approach

3. Internal Models Approach

B. Advanced Approach

C. Market Risk Management

XI. Operational Risk Capital

XII. Impact of the Enterprise Capital Rule

A. Enterprise-Wide

B. Single-Family Business

C. Multifamily Business

D. Other Assets

XIII. Comparisons to the U.S. Banking Framework

XIV. Compliance Period

XV. Temporary Increases of Minimum Capital Requirements and Other Conforming Amendments

XVI. Paperwork Reduction Act

XVII. Regulatory Flexibility Act

XVIII. Proposed Rule

I. Introduction

FHFA is seeking comments on a new regulatory capital framework for the Enterprises. This notice of proposed rulemaking (proposed rule) is a re-proposal of the regulatory capital framework set forth in the notice of proposed rulemaking published in the Federal Register on July 17, 2018 (2018 proposal).[1] The 2018 proposal, which remains the foundation of the proposed rule, contemplated risk-based capital requirements based on a granular assessment of credit risk specific to different mortgage loan categories, as well as two alternatives for an updated leverage ratio requirement. With this re-proposal, FHFA is proposing enhancements to establish a post-conservatorship regulatory capital framework that ensures that each Enterprise operates in a safe and sound manner and is positioned to fulfill its statutory mission to provide stability and ongoing assistance to the secondary mortgage market across the economic cycle, in particular during periods of financial stress.[2]

Pursuant to the Federal Housing Enterprises Financial Safety and Soundness Act of 1992 [3] (Safety and Soundness Act), as amended by the Housing and Economic Recovery Act of 2008 [4] (HERA), the FHFA Director's principal duties include, among other duties, ensuring that each Enterprise operates in a safe and sound manner, that the operations and activities of each Enterprise foster liquid, efficient, competitive, and resilient national housing finance markets, and that each Enterprise carries out its statutory mission only through activities that are authorized under and consistent with the Safety and Soundness Act and its charter.[5] Pursuant to their charters, the statutory purposes of the Enterprises are, among other purposes, to provide stability in, and ongoing assistance to, the secondary market for residential mortgages.[6] Consistent with these statutory duties and purposes, FHFA's enhancements contemplated by the proposed rule are intended to achieve three primary objectives:

- Preserve the mortgage risk-sensitive framework of the 2018 proposal, with simplifications and refinements;

- Increase the quantity and quality of the regulatory capital of the Enterprises to ensure that, during and after conservatorship, each Enterprise operates in a safe and sound manner and is positioned to fulfill its statutory mission to provide stability and ongoing assistance to the secondary mortgage market across the economic cycle; and

- Address the pro-cyclicality of the risk-based capital requirements of the 2018 proposal, also in furtherance of the safety and soundness of the Enterprises and their countercyclical mission.

FHFA believes it is important to re-propose the regulatory capital framework to afford interested parties an opportunity to comment on the enhancements contemplated by the proposed rule in its entirety in light of FHFA's intent to responsibly end the conservatorships of the Enterprises. This policy change is a departure from FHFA's stated policy at the time of the 2018 proposal, when the prospects for indefinite conservatorships might have informed the expectations of interested parties, their decision to comment, and the nature of comments submitted. Despite this, the comments received on the 2018 proposal were valuable and important. FHFA emphasizes that the purpose of the proposed rule is to establish a regulatory capital framework that ensures the safety and soundness of each Enterprise and its ability to fulfill its statutory mission across the economic cycle.

II. Overview of the Proposed Rule

A. Regulatory Capital Requirements

In response to the comments and feedback on the 2018 proposal and in furtherance of FHFA's stated objectives, the regulatory capital framework contemplated by the proposed rule would require each Enterprise to maintain the following risk-based capital:

- Total capital not less than 8.0 percent of risk-weighted assets, determined as described below;

- Adjusted total capital not less than 8.0 percent of risk-weighted assets;

- Tier 1 capital not less than 6.0 percent of risk-weighted assets; and

- Common equity tier 1 (CET1) capital not less than 4.5 percent of risk-weighted assets.

Each Enterprise also would be required to satisfy the following leverage ratios:

- Core capital not less than 2.5 percent of adjusted total assets; and

- Tier 1 capital not less than 2.5 percent of adjusted total assets.

Adjusted total assets would be defined as total assets under generally accepted accounting principles (GAAP), with adjustments to include certain off-balance sheet exposures. Total capital and core capital would have the meaning given in the Safety and Soundness Act. Adjusted total capital, tier 1 capital, and CET1 capital would be defined based on the definitions of total capital, tier 1 capital, and CET1 capital set forth in the regulatory capital framework (the Basel framework) developed by the Basel Committee on Bank Supervision (BCBS) that is the basis for the United States banking regulators' regulatory capital framework (U.S. banking framework). These supplemental regulatory capital definitions would fill certain gaps in the statutory definitions of core capital and total capital by making customary deductions and other adjustments for certain deferred tax assets (DTAs), goodwill, intangibles, and other assets that tend to have less loss-absorbing capacity during a financial stress.

To calculate its risk-based capital requirements, an Enterprise would determine its risk-weighted assets under two approaches—a standardized approach and an advanced approach—with the greater of the two used to determine its risk-based capital requirements. Under both approaches, an Enterprise's risk-weighted assets would equal the sum of its credit risk-weighted assets, market risk-weighted assets, and operational risk-weighted assets.

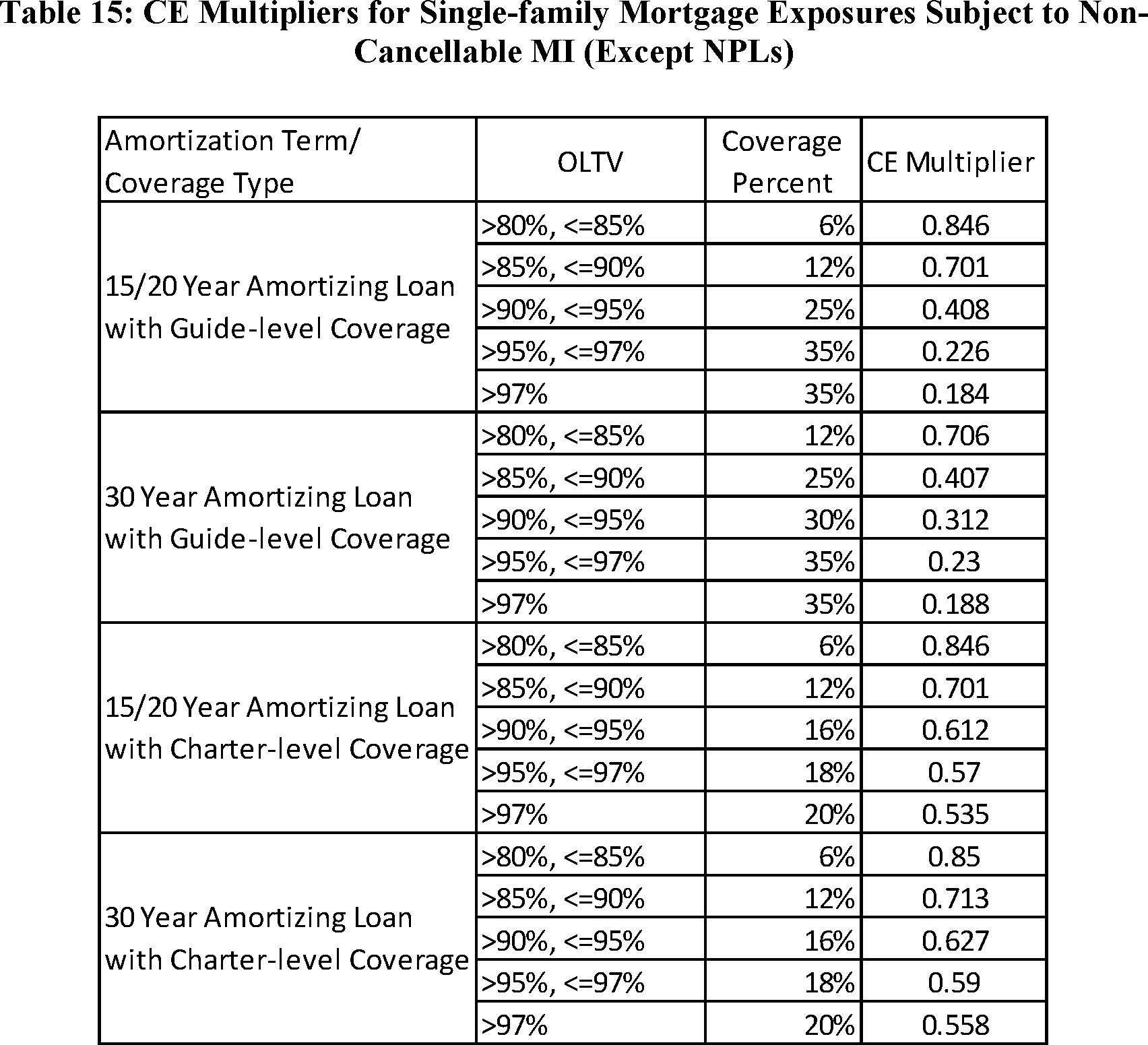

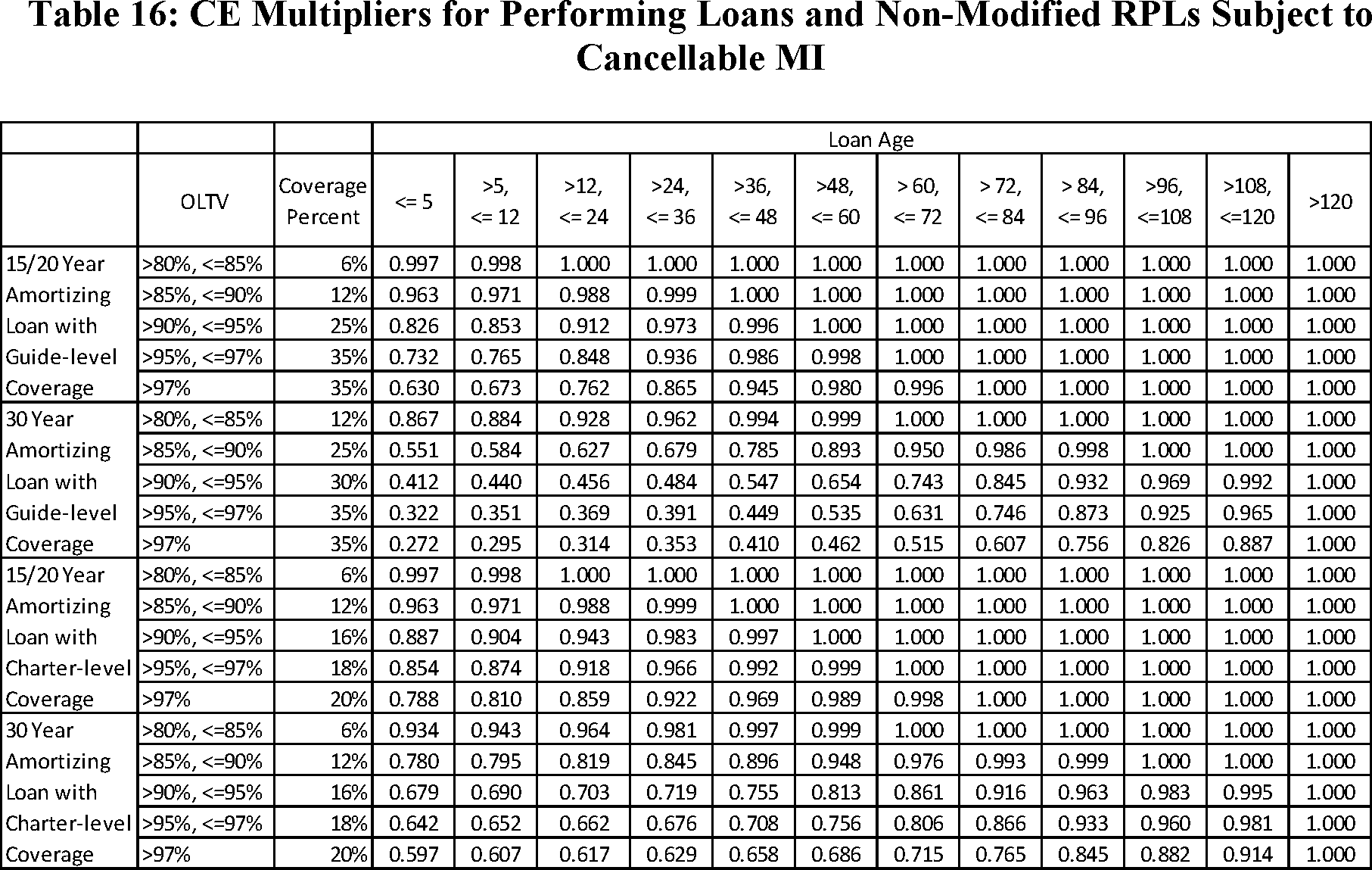

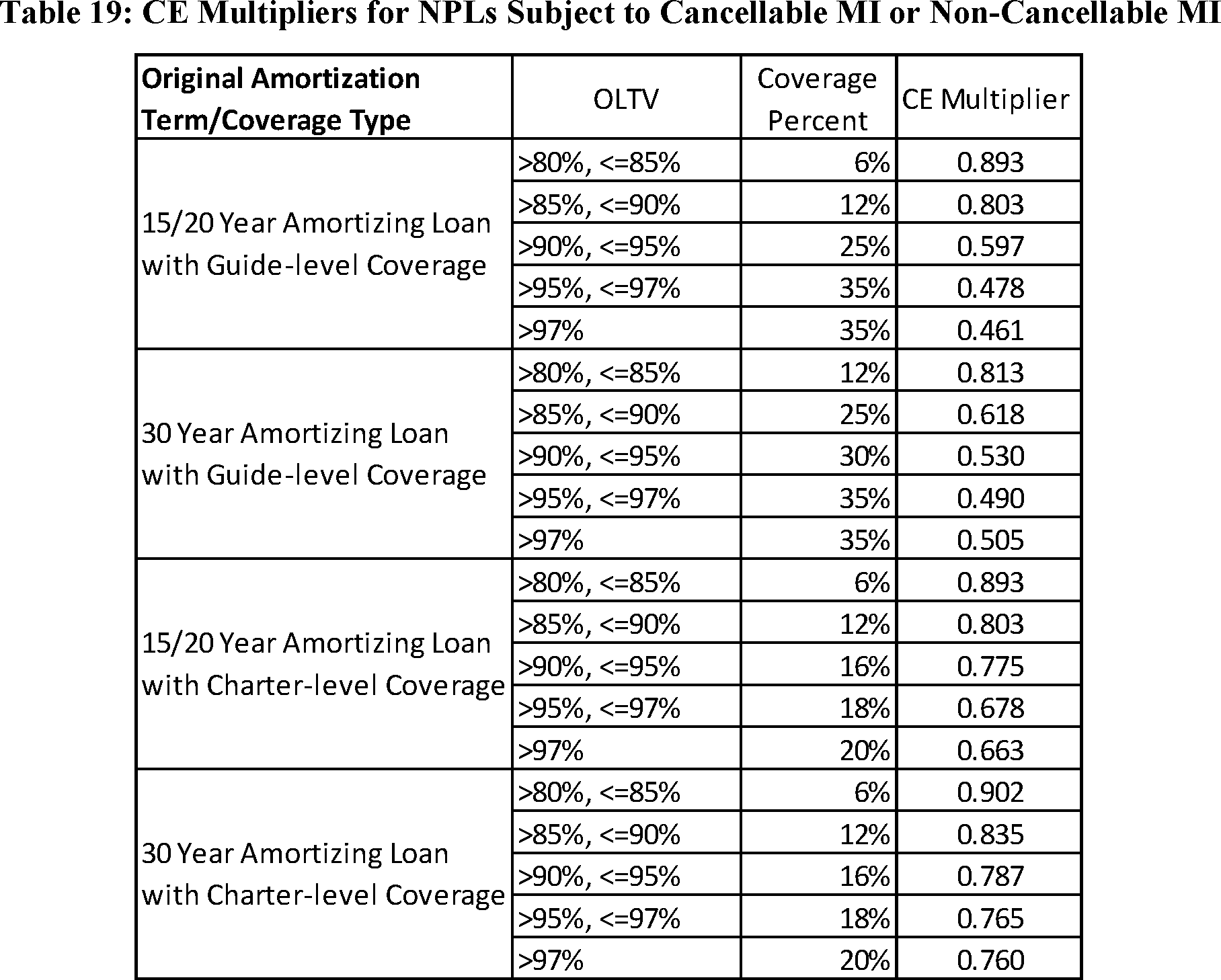

Under the standardized approach, the credit risk-weighted assets for mortgage loans secured by 1-4 unit residences (single-family mortgage exposures) and mortgage loans secured by five or more unit residences (multifamily mortgage exposures) would be determined using lookup grids and multipliers that assign an exposure-specific risk weight based on the risk characteristics of the mortgage exposure. The underlying exposure-specific credit risk capital requirements generally would be similar to those in the grids and multipliers of the 2018 proposal, subject to some simplifications and refinements discussed in Sections VIII.A and VIII.B.[7]

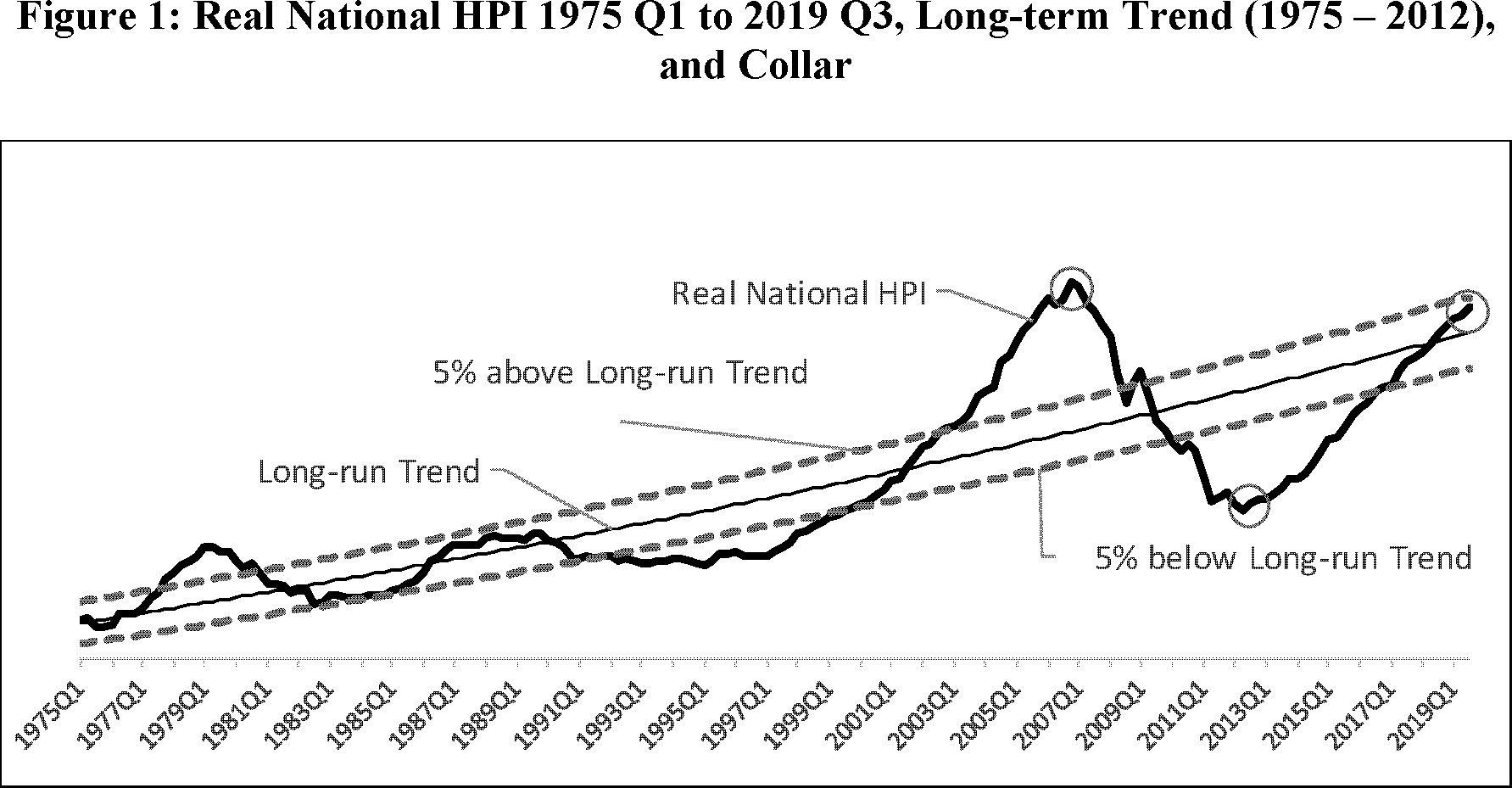

Like the 2018 proposal, the base risk weight would be a function of the mortgage exposure's loan-to-value (LTV) ratio with the property value generally marked to market (MTMLTV). For single-family mortgage exposures, the MTMLTV would be subject to a countercyclical adjustment to the extent that national house prices are 5.0 percent greater or less than an inflation-adjusted long-term trend. For both single-family and multifamily mortgage exposures, this base risk weight would then be adjusted to reflect additional risk attributes of the mortgage exposure and any loan-level credit enhancement, with the associated risk multipliers also generally similar to those of the 2018 proposal. To ensure an appropriate level of capital, this adjusted risk weight would be subject to a minimum floor of 15 percent.

As of September 30, 2019, under the proposed rule's standardized approach, the Enterprises' average risk weight for single-family mortgage exposures would have been 26 percent, and the Enterprises' average risk weight for multifamily mortgage exposures would have been 51 percent.[8] The average risk weights for single-family and multifamily mortgage exposures originated and acquired by an Enterprise in the previous six months would have been approximately 36 percent and 67 percent, respectively.[9]

While the standardized approach would utilize FHFA-prescribed lookup grids and risk multipliers, the advanced approach for credit risk-weighted assets would rely on each Enterprise's internal models. The advanced approach requirements would require each Enterprise to maintain its own processes for identifying and assessing credit risk, market risk, and operational risk. These requirements should ensure that each Enterprise continues to enhance its risk management system and also that neither Enterprise simply relies on the standardized approach's lookup grids and multipliers to define credit risk tolerances, measure its credit risk, or allocate capital. In the course of FHFA's supervision of each Enterprise's internal models for credit risk, FHFA also could identify opportunities to update or otherwise enhance the standardized approach's lookup grids and multipliers in a future rulemaking.

Under both the standardized and advanced approaches, an Enterprise would determine the capital treatment for eligible credit risk transfers (CRT) under a securitization framework by assigning risk weights to retained CRT exposures. Under the standardized approach, tranche-specific risk weights would be subject to a 10 percent floor. The proposed rule seeks comment on two approaches to determining the risk-weighted assets for retained CRT exposures, one of which contemplates adjustments to the exposure amounts of the retained CRT exposures to reflect counterparty risk, loss timing risk, and a general adjustment for the differences between CRT and regulatory capital, and the other of which is based on the U.S. banking framework.

Each Enterprise also would determine a market risk capital requirement for spread risk. Market risks other than spread risk would not be assigned a market risk capital requirement, but FHFA is seeking comment on more comprehensive approaches. Under the standardized approach, an Enterprise would determine its market risk-weighted assets using FHFA-specified formulas for some covered positions and its own models for other covered positions. An Enterprise would separately determine its market risk-weighted assets under an advanced approach that relies only on its own internal models for all covered positions.

The proposed rule also would require each Enterprise to determine its operational risk capital requirement utilizing the U.S. banking framework's advanced measurement approach, subject to a floor equal to 15 basis points of the Enterprise's adjusted total assets.

Each of these risk-based and leverage ratio requirements would be enforceable by FHFA under its general authority to order an Enterprise to cease and desist from a violation of law, which would include the proposed rule and its regulatory capital requirements. Pursuant to that authority, FHFA may require an Enterprise to develop and implement a capital restoration plan or take other appropriate corrective action. FHFA also could elect to enforce the risk-based and leverage ratio requirements pursuant to its authority to require an Enterprise to develop a plan to achieve compliance with prescribed prudential management and operational standards, and FHFA also could enforce the core capital leverage ratio requirement or the risk-based total capital requirement pursuant to its separate authority to require prompt corrective action if an Enterprise fails to maintain certain prescribed regulatory levels.

B. Capital Buffers

To avoid limits on capital distributions and discretionary bonus payments, an Enterprise would have to maintain regulatory capital that exceeds each of its adjusted total capital, tier 1 capital, and CET1 capital requirements by at least the amount of its prescribed capital conservation buffer amount (PCCBA). That PCCBA would consist of three separate component buffers—a stress capital buffer, a countercyclical capital buffer, and a stability capital buffer.

- The stress capital buffer would be 0.75 percent of the Enterprise's adjusted total assets, with this buffer in effect replacing the 2018 proposal's going-concern buffer. The 2018 proposal's going-concern buffer was a part of the Enterprise's total capital requirement, such that an Enterprise would be subject to enforcement action if it drew down this going-concern buffer. In contrast, under the proposed rule, drawing down the stress capital buffer generally would trigger only limits on capital distributions and discretionary bonus payments. By prescribing less severe sanctions for drawing down this buffer during a period of financial stress, the proposed rule's approach should help position an Enterprise to fulfill its statutory mission across the economic cycle and also dampen the pro-cyclicality of the aggregate risk-based capital requirements. FHFA is also seeking comment on whether to periodically re-size the stress capital buffer, similar to the approach recently adopted by the U.S. banking regulators,[10] to the extent that FHFA's eventual program for supervisory stress tests determines that an Enterprise's peak capital exhaustion under a severely adverse stress would exceed 0.75 percent of adjusted total assets.

- The countercyclical capital buffer amount initially would be set at 0 percent of the Enterprise's adjusted total assets. FHFA does not expect to adjust this buffer in the place of, or to supplement, the countercyclical adjustment to the risk-based capital requirements. Instead, as under the Basel and U.S. banking frameworks, FHFA would adjust the countercyclical capital buffer taking into account the macro-financial environment in which the Enterprises operate, such that it would be deployed only when excess aggregate credit growth is judged to be associated with a build-up of system-wide risk. This focus on excess aggregate credit growth means the countercyclical buffer likely would be deployed on an infrequent basis, and generally only when similar buffers are deployed by the U.S. banking regulators.

- An Enterprise's stability capital buffer would be tailored to the risk that the Enterprise's default or other financial distress could have on the liquidity, efficiency, competitiveness, or resiliency of national housing finance markets. FHFA is proposing a stability capital buffer based on the Enterprise's share of residential mortgage debt outstanding, and seeking comment on an alternative based on the U.S. banking framework's methodology. Under either methodology, the stability capital buffer would be a percent of adjusted total assets. Under the market share approach, as of September 30, 2019, Freddie Mac's and Fannie Mae's stability capital buffers would have been, respectively, 0.64 and 1.05 percent of adjusted total assets.

Fixing the PCCBA at a specified percent of an Enterprise's adjusted total assets, instead of risk-weighted assets, is a notable departure from the Basel framework. FHFA intends a fixed-percent PCCBA, among other things, to reduce the impact that the PCCBA potentially could have on higher risk exposures, to avoid amplifying the secondary effects of any model or similar risks inherent to the calibration of granular risk weights for mortgage exposures, and to further mitigate the pro-cyclicality of the aggregate risk-based capital requirements.

Finally, to avoid limits on capital distributions and discretionary bonus payments, the Enterprise also would be required to maintain tier 1 capital in excess of the amount required under its tier 1 leverage ratio requirement by at least the amount of its prescribed leverage buffer amount (PLBA). The PLBA would equal 1.5 percent of the Enterprise's adjusted total assets, such that the PLBA-adjusted leverage ratio requirement would remain a credible backstop to the PCCBA-adjusted risk-based capital requirements.

C. Key Enhancements

The proposed rule contemplates a number of key enhancements to the 2018 proposal, including:

- Simplifications and refinements of the grids and risk multipliers for the credit risk capital requirements for single-family mortgage exposures, including removal of the single-family risk multipliers for loan balance and the number of borrowers.

- A countercyclical adjustment to the credit risk capital requirements for single-family mortgage exposures.

- A prudential floor on the credit risk capital requirement for mortgage exposures.

- Refinements to the capital treatment of CRT structures, including a minimum capital requirement on senior tranches of CRT retained by an Enterprise and an adjustment to reflect that CRT does not have the same loss-absorbing capacity as equity capital.

- The addition of a credit risk capital requirement for Enterprise crossholdings of mortgage-backed securities (MBS).

- Risk-based capital requirements for a number of other exposures not explicitly addressed by the 2018 proposal.

- Supplemental capital requirements based on the Basel framework's definitions of total capital, tier 1 capital, and CET1 capital.

- Capital buffers that would subject an Enterprise to increasing limits on capital distributions and discretionary bonus payments to the extent that its regulatory capital falls below the prescribed buffer amounts.

- A stability capital buffer tailored to the risk that an Enterprise's default or other financial distress could have on the liquidity, efficiency, competitiveness, and resiliency of national housing finance markets.

- A revised method for determining operational risk capital requirements, as well as a higher floor.

- A requirement that each Enterprise maintain internal models for determining its own estimates of risk-based capital requirements.

D. Sizing of Regulatory Capital Expectations

1. Aggregate Regulatory Capital

Table 1 details how much regulatory capital the Enterprises together would have been required to maintain under the proposed rule as of September 30, 2019 to avoid restrictions on capital distributions and discretionary bonus payments.[11]

Table 1 shows a combined Enterprise statutory total risk-based capital requirement of $135 billion (8 percent of risk-weighted assets). The statutory risk-based capital framework does not include any capital buffers. In contrast, the supplementary risk-based capital framework includes three capital requirements (CET1, tier 1, and adjusted total capital) along with three capital buffers (countercyclical, stress capital, and stability) that comprise the PCCBA. While the capital buffers are not strictly a capital requirement, they would materially increase the regulatory capital that each Enterprise would have to maintain to avoid restrictions on capital distributions and discretionary bonuses.

Focusing on high-quality capital, the combined Enterprise CET1 capital requirement was $76 billion (4.5 percent of risk-weighted assets), the tier 1 capital requirement was $101 billion (6 percent of risk-weighted assets), and the adjusted total capital requirement was $135 billion (8 percent of risk-weighted assets). The combined PCCBA was $99 billion, comprising the $46 billion stress capital buffer, $53 billion stability capital buffer, and $0 countercyclical capital buffer. The capital requirements and PCCBA totaled $175 billion for CET1 capital, $200 billion for tier 1 capital, and $234 billion for adjusted total capital. A more nuanced look at the importance of high-quality capital, and specifically how the Enterprises' supplemental capital measures would have evolved in relation to their statutory capital measures leading up to the 2008 financial crisis, is included in Section III.B.3.

Table 1 then shows a combined leverage ratio requirement of $152 billion under the proposed rule. Both the core capital and supplementary tier 1 leverage ratio requirements are equal to 2.5 percent of adjusted total assets, so there is no difference between the two leverage ratio requirements. However, there are important differences between core capital and tier 1 capital related to the loss-absorbing capacity of each capital metric, as discussed in Section V.B.

The supplementary framework also includes a tier 1 capital PLBA equal to 1.5 percent of adjusted total assets, or $91 billion for the Enterprises combined. In aggregate, the Enterprises' combined tier 1 leverage ratio requirement and PLBA would have been $243 billion as of September 30, 2019.

2. 2018 Proposal's Capital Requirements

Table 2 presents estimates of the Enterprises' combined regulatory capital under the proposed rule broken out by risk category and asset category as of September 30, 2019. Table 2 also presents estimates of the Enterprises' combined capital requirements under the 2018 proposal, both as of September 30, 2017—the as-of date in the 2018 proposal—and as of September 30, 2019.[12]

Table 2 shows an estimated combined risk-based capital requirement of $135.1 billion, or 2.22 percent of the Enterprises' adjusted total assets, under the proposed rule as of September 30, 2019, then provides a further breakdown by risk category. Net credit risk capital accounts for $134.9 billion before CRT and $112.8 billion after CRT, market risk capital accounts for $13.6 billion, and operational risk capital accounts for $8.7 billion. The DTA requirement is zero as of September 30, 2019.

Using the same September 30, 2019 portfolio date, the combined risk-based capital requirement under the 2018 proposal would have been similar to the combined risk-based capital requirement under the proposed rule. The differences in required regulatory capital between the two proposals are in post-CRT net credit risk capital (+45.0 billion), removal of the going-concern buffer (−$43.5 billion), operational risk (+$4.1 billion), and DTA (−$7.4 billion). The capital requirement for market risk was unchanged. Primary drivers of the $45.0 billion increase in post-CRT net credit risk capital are a new prudential floor on the credit risk capital requirement for mortgage exposures and refinements to the capital treatment of CRT structures, including a minimum capital requirement on senior tranches of CRT retained by an Enterprise. A caveat to this comparison is that the 2018 proposal increased the total capital requirement by a DTA offset, while the proposed rule, consistent with the Basel framework, proposes instead to deduct the amount of that DTA offset from CET1 capital (and therefore tier 1 and adjusted total capital). The 2018 proposal's $136.9 billion combined risk-based capital requirement would have been, in effect, $129.5 billion under the DTA approach of the proposed rule.

In contrast to the 2018 proposal, the proposed rule includes a set of three buffers that would materially increase the regulatory capital that each Enterprise would have to maintain to avoid restrictions on capital distributions and discretionary bonuses. The proposed rule's stress capital buffer of $45.5 billion replaces the 2018 proposal's $43.5 billion going-concern buffer, and is complemented by the stability capital buffer of $53.3 billion and the countercyclical capital buffer that is currently set to zero. The three buffers in aggregate form the PCCBA, which totals $98.8 billion for the Enterprises combined, or 1.63 percent of the adjusted total assets. The aggregate risk-based capital requirement and PCCBA is a combined $234.3 billion under the proposed rule, or 3.86 percent of the Enterprises' adjusted total assets.

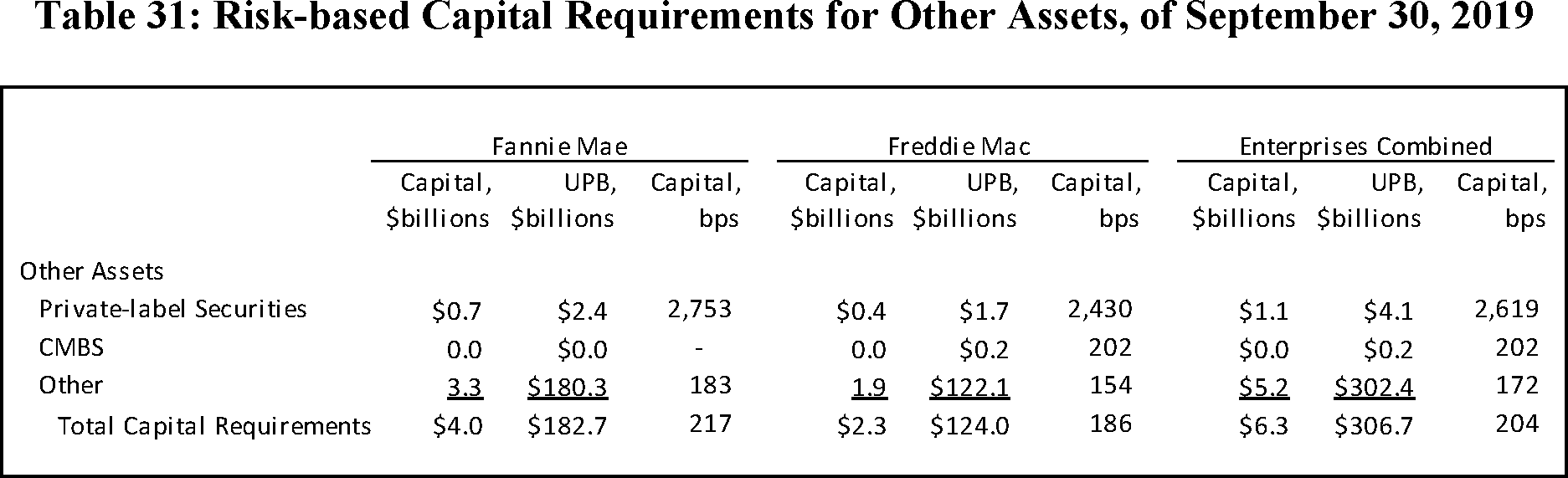

Table 3 again shows an estimated combined risk-based capital requirement of $135.1 billion, or 2.22 percent of the Enterprises' adjusted total assets under the proposed rule as of September 30, 2019, then provides a further breakdown by asset category. The Enterprises' combined risk-based capital requirement for single-family mortgage exposures is $111.0 billion under the proposed rule, while the combined risk-based capital requirement for multifamily mortgage exposures is $17.8 billion. In addition, the combined risk-based capital requirements for DTA and other assets under the proposed rule is zero and $6.3 billion, respectively.

Excluding the going-concern buffer, which was a capital requirement in the 2018 proposal but has been replaced by the stress capital buffer in the proposed rule, the combined risk-based capital requirements under the 2018 proposal for the single-family and multifamily businesses were $67.8 billion and $12.2 billion, respectively, as of September 30, 2019. As discussed above and shown in Table 3, the enhancements in the proposed rule would have increased the required capital for single-family assets and multifamily assets by $43.2 billion and $5.6 billion, respectively. Similarly, the risk-based capital requirement for other assets has increased by $0.2 billion. Finally, the risk-based capital requirement for DTA decreased by $7.4 billion in the proposed rule due to its new capital treatment.

The pro-cyclicality of the 2018 proposal's risk-based capital requirements complicates comparisons to the proposed rule. Under the 2018 proposal, the Enterprises would have likely found it necessary to maintain a considerable capital surplus in anticipation of a financial stress. One Enterprise's comment letter suggested that its total capital requirement would be expected to increase as much as 80

percent in a severely adverse stress.[13] The amount of this managerial cushion would have depended on the extent to which the Enterprises viewed it to be potentially costly or difficult to raise new capital in the midst of a financial stress.[14] The 2018 proposal's enforcement framework amplified the necessity of a managerial cushion by incorporating the going-concern buffer into the capital requirements, a violation of which could trigger significant regulatory sanctions. In contrast, the proposed rule converts the going-concern buffer into a stress capital buffer that an Enterprise may draw down during a period of financial stress. Because a managerial cushion in anticipation of an eventual stress would have been a practical, if not legal, necessity for the Enterprises, comparisons to the 2018 proposal should start with a reasonable assumption regarding the amount of this capital surplus.[15]

FHFA is cognizant that the leverage ratio requirements would currently exceed the risk-based capital requirements. FHFA has settled on this calibration of the leverage ratio requirements after considerable deliberation. The leverage ratio requirements are intended to serve as non-risk-based measures that provide a credible backstop to the risk-based capital requirements to safeguard against model risk and measurement error with a simple, transparent, independent measure of risk. The leverage ratio requirements would have the added benefit of dampening some of the pro-cyclicality inherent in the risk-based capital requirements. As discussed in Section VI.B.3, FHFA has sized the leverage ratio requirements to be a credible backstop to the risk-based capital requirements, taking into account considerations relating to the Enterprises' historical loss experiences, the model and related risks posed by the calibration of the risk-based capital requirements, and the analogous leverage ratio requirements under the U.S. banking framework and of the Federal Home Loan Banks. If the leverage ratio requirements are to be a credible backstop, there will inevitably be periods when leverage ratio requirements require more regulatory capital than the risk-based capital requirements, as is the case as of September 30, 2019. FHFA believes that mortgage market conditions as of September 30, 2019 reflect circumstances consistent with a period under which a credible leverage ratio would be binding, given the exceptional single-family house price appreciation since 2012, the unemployment rate at an historically low level, the strong credit performance of mortgage exposures as of that time, the significant progress by the Enterprises to materially reduce legacy exposure to non-performing loans (NPLs) and re-performing loans, robust CRT market access enabling substantial risk transfer, and the generally strong condition of key counterparties, such as mortgage insurers.

3. 2008 Financial Crisis Loss Experience 16

This section examines the peak cumulative capital losses of each Enterprise relative to several different regulatory capital metrics: The statutory risk-based and leverage ratio requirements applicable to the Enterprise in 2007; the aggregate risk-based capital (requirement plus the PCCBA) under the proposed rule but without the contemplated single-family countercyclical adjustment; and the aggregate leverage capital (requirement plus the PLBA) under the proposed rule but without the contemplated single-family countercyclical adjustment.17 As discussed in Section IV.B.2, under the 2018 proposal, Fannie Mae's and Freddie Mac's peak losses would have left, respectively, only $3 billion and $12 billion in remaining capital, not enough to have sustained the market confidence necessary for either Enterprise to continue as a going concern.

Table 4 shows that as of December 31, 2007, Fannie Mae's statutory risk-based capital requirement was $25 billion, or 0.8 percent of adjusted total assets. The Enterprise's statutory minimum leverage ratio requirement was $42 billion, or 1.4 percent of adjusted total assets. For comparison, as of the same date, Fannie Mae's proposed risk-based measures (adjusted total capital requirement plus PCCBA) would have been $209 billion or 6.9 percent of adjusted total assets, and the proposed leverage measures (leverage ratio requirement plus PLBA) would have been $122 billion or 4.0 percent of adjusted total assets. While the leverage measure would have fallen $45 billion short of Fannie Mae's peak cumulative capital losses of $167 billion (5.5 percent of adjusted total assets), the proposed risk-based measures would have exceeded those peak losses by $42 billion. These comparisons are subject to the caveat that Fannie Mae's $167 billion in peak cumulative capital losses include a valuation allowance on DTAs of $64 billion. Because much of Fannie Mae's DTAs would have been deducted from adjusted total capital and tier 1 capital, the adjusted total capital and tier 1 capital that actually would have been exhausted during the 2008 financial crisis would have been considerably less than the $167 billion in peak cumulative capital losses reflected in Table 4.

Table 5 shows that as of December 31, 2007, Freddie Mac's statutory risk-based capital requirement was $14 billion, or 0.6 percent of adjusted total assets. The Enterprise's statutory minimum leverage ratio requirement was $34 billion, or 1.6 percent of adjusted total assets. For comparison, as of the same date, Freddie Mac's proposed risk-based measures (adjusted total capital requirement plus PCCBA) would have been $128 billion or 5.9 percent of adjusted total assets, and the proposed leverage measures (leverage ratio requirement plus PLBA) would have been $87 billion or 4.0 percent of adjusted total assets. While the leverage measure would have fallen $11 billion short of Freddie Mac's peak cumulative capital losses of $98 billion (4.5 percent of adjusted total assets), the proposed risk-based measures would have exceeded those peak losses by $30 billion. These comparisons are subject to the caveat that Freddie Mac's $98 billion in peak cumulative capital losses include a valuation allowance on DTAs of $34 billion. Because much of Freddie Mac's DTAs would have been deducted from adjusted total capital and tier 1 capital, the adjusted total capital and tier 1 capital that actually would have been exhausted during the 2008 financial crisis would have been considerably less than the $98 billion in peak cumulative capital losses reflected in Table 5.

As discussed in Section VIII.A.4, FHFA is proposing that the base risk weights for single-family mortgage exposures would be subject to a countercyclical adjustment due to MTMLTV adjustments an Enterprise would be required to make when national house prices deviate by more than 5.0 percent above or below an estimated inflation-adjusted long-term trend. It is important to note that any additional regulatory capital that would have been required under the proposed single-family countercyclical adjustment is not included in the estimates of regulatory capital in either Tables 4 or 5. Looking back, it is likely that, given the considerable house price appreciation in the decade before the financial crisis, this countercyclical adjustment would have been in effect as of December 31, 2007. However, there are too many unknowns to quantify with any reasonable degree of certainty what that effect would have been, how the Enterprises' actions might have changed because of it, and how changes in the actions of the Enterprises might have affected the overall market. Therefore, FHFA is presenting the estimates without including a countercyclical adjustment, and acknowledging that with the countercyclical adjustment in place, the Enterprises would likely have had an even larger capital surplus relative to their peak cumulative capital losses than is presented in Tables 4 and 5.

III. Background

A. Pre-Crisis Regulatory Capital Framework

The Safety and Soundness Act established FHFA's predecessor agency, the Office of Federal Housing Enterprise Oversight (OFHEO), as the safety and soundness regulator of the Enterprises. As originally enacted, the Safety and Soundness Act specified a minimum capital requirement for the Enterprises in the form of a leverage ratio requirement set in statute at an amount equal to the sum of 2.5 percent of on-balance sheet assets and 0.45 percent of credit guarantees of MBS held by outside investors. OFHEO did not have the authority to adjust this minimum capital requirement.

The Safety and Soundness Act also required OFHEO to establish by regulation a risk-based capital stress test such that each Enterprise could survive a ten-year period with credit losses arising out of a prolonged regional stress [18] and large movements in interest rates.[19] Over a 7-year period, OFHEO issued a series of Federal Register notices to solicit public comments on the risk-based capital stress test regulation, eventually finalizing the rule in 2001. The final risk-based capital requirements, however, had little practical impact. The capital required under the statutory leverage ratio requirement consistently exceeded the capital required under OFHEO's risk-based regulation, in large part due to the prescriptive restrictions imposed by statute on the underlying stress scenario and also due to model risk-related failures to update the underlying data and model calibrations.[20] This pre-crisis regulatory capital framework would soon prove inadequate.

B. Lessons of the 2008 Financial Crisis

Starting in 2006, house prices in some regional markets began to decline, mortgage defaults began to rise, and the Enterprises began to incur credit and mark-to-market losses. In 2007, housing price declines spread across the nation, and issuances of private-label securities (PLS) largely ceased. The Enterprises' losses continued to mount into 2008, their share prices rapidly fell, and the spreads on their unsecured debt and mortgage-backed securities (MBS) widened.

In July 2008, following growing concern about the Enterprises' solvency, Congress passed HERA, establishing FHFA as the regulator for the Enterprises and authorizing the Treasury Department to support the Enterprises through purchases of their obligations and other securities. On September 6, 2008, FHFA used its new authorities under HERA to place each Enterprise into conservatorship. The next day, the Treasury Department exercised its HERA authority to enter into Senior Preferred Stock Purchase Agreements (each a PSPA) to support the Enterprises. The Enterprises ultimately required $191.5 billion in cash draws from the Treasury Department under the PSPAs.

1. Capital Adequacy

The scale of the Enterprises' capital exhaustion during the 2008 financial crisis is critically relevant to the capital necessary to ensure that each Enterprise operates in a safe and sound manner and is positioned to fulfill its statutory mission across the economic cycle.

As discussed in Section II.D.3, the Enterprises' crisis-era cumulative capital losses peaked at $265 billion, approximately 4.8 percent of their total assets as of December 31, 2007. Setting aside the valuation allowances on their DTAs, which are subject to deductions and other adjustments to regulatory capital under the proposed rule, the Enterprises' peak cumulative capital losses were $167 billion, approximately 3.0 percent of their total assets as of December 31, 2007.

The Enterprises' crisis-era cumulative capital losses, while significant, could have been greater. The Enterprises' losses were likely mitigated by unprecedented federal government support of the housing market and the economy during the crisis, including the Home Affordable Modification Program, the Troubled Asset Relief Program, the 2009 stimulus package,[21] and the Federal Reserve System's purchases of more than $1.2 trillion of the Enterprises' debt and MBS from January 2009 to March 2010. The Enterprises' losses also were likely dampened by the declining interest rate environment of the period, when the interest rates on 30-year fixed-rate mortgage loans declined by approximately 200 basis points through the end of 2011, facilitating re-financings and loss mitigation programs.[22]

The Enterprises did later recoup a portion of the underlying valuation adjustments and other losses. However, peak cumulative capital losses are relevant to assessing the amount of capital that creditors and other counterparties would require to regard the Enterprises as viable going concerns throughout the duration of another severe economic downturn. Indeed, the Enterprises were still operating and able to recoup some of these losses only because the Treasury Department's support through the PSPAs kept them solvent going concerns.

2. Going-Concern Standard

The Enterprises' crisis-era funding difficulties established that each Enterprise must be capitalized to remain a viable going concern both during and after a severe economic downturn. Calibrating capital adequacy based on “claims paying capacity” or an insurance-like or similar standard that does not emphasize a going-concern standard is inconsistent with this lesson of the crisis in at least two respects.

First, the Enterprises fund themselves with a significant amount of short-term unsecured debt that must be regularly refinanced. Each Enterprise's funding needs are very likely to increase during an economic downturn, all else equal, as the Enterprise funds purchases of NPLs out of securitization pools. This is a funding need that peaked at $345 billion in 2010.

These ordinary course and pro-cyclical funding needs can be met only if the Enterprise continues to be regarded as a viable going concern by creditors throughout the duration of a financial stress. Creditors will be most skeptical of an Enterprise's continued solvency during periods of market turmoil, and it was the increase in the Enterprises' borrowing costs and the associated difficulties that the Enterprises faced in refinancing their debt that were among the most immediate grounds for FHFA placing the Enterprises into conservatorship.[23]

Second, only a going-concern capital adequacy standard can ensure that each Enterprise will be positioned to fulfill its statutory mission to provide stability and ongoing assistance to the secondary mortgage market across the economic cycle. The Enterprises were not positioned to effectively support the secondary mortgage market as their financial conditions deteriorated in 2007 and 2008.[24] In an attempt to enable the Enterprises to continue to support the secondary mortgage market, OFHEO relaxed the mortgage portfolio caps and reduced a capital buffer that had been imposed by consent order.[25]

3. High-Quality Capital

Another lesson of the 2008 financial crisis is that it is not only the quantity but also the quality of the regulatory capital, especially its loss-absorbing capacity, that is critical to the Enterprises' safety and soundness. Market confidence in the Enterprises came into doubt in mid-2008 when Fannie Mae and Freddie Mac had total capital of, respectively, $55.6 billion and $42.9 billion. Questions about the Enterprises' solvency likely arose in part due to their sizeable DTAs, which counted toward total capital but had less loss-absorbing capacity during a period of negative income. Freddie Mac would have actually had a negative book value as of June 30, 2008 after deducting its DTAs. Besides the DTA valuation allowances, there was also uncertainty as to the sufficiency of the Enterprises' allowances for loan losses (ALLL).[26] For these and other reasons, the Basel framework includes deductions and other adjustments for DTAs and ALLL, as well as other capital elements that might have less loss-absorbing capacity.[27]

Table 6 illustrates the importance of requiring high-quality capital by showing the evolution of CET1 capital, tier 1 capital, adjusted total capital, core capital, and total capital at each Enterprise leading up to the 2008 financial crisis. As the table indicates, the Enterprises' combined core capital increased from $77.3 billion in 2006 to $84.1 billion in 2008, suggesting at first glance a position of some financial strength. However, over the same time period the Enterprises' combined tier 1 capital decreased markedly from $76.3 billion to $24.1 billion, indicating a capital position with deteriorating and substantially less loss-absorbing capacity. Similarly, the Enterprises' combined total capital increased from $78.7 billion in 2006 to $98.5 billion in 2008, while over the same time period the Enterprises' adjusted total capital decreased from $85.9 billion to $29.6 billion.

4. Stability of the National Housing Finance Markets

After the taxpayer-funded rescue of the Enterprises in 2008, there can be no doubt as to the risk posed by an insolvent or otherwise financially distressed Enterprise to the stability of the national housing finance markets. The Enterprises were then, and remain today, the dominant participants in the housing finance system, owning or guaranteeing 37 percent of residential mortgage debt outstanding as of December 31, 2007 and 44 percent of residential mortgage debt outstanding as of September 30, 2019. Both then and still today, banks, insurance firms, and securities broker-dealers own significant amounts of the Enterprises' unsecured debt and MBS. Both then and still today, the Enterprises control critical infrastructure for securitizing and administering $5.5 trillion of outstanding single-family and multifamily conventional MBS.[28] Given the nature, scope, size, scale, concentration, and interconnectedness of each Enterprise, the financial distress of an Enterprise could have significant adverse effects on the liquidity, efficiency, competitiveness, or resiliency of national housing finance markets. For these and related reasons, the Treasury Department ultimately invested $191.5 billion under the PSPAs in the Enterprises to keep them solvent going concerns.

C. Post-Crisis Changes to Regulatory Capital Frameworks

After the 2008 financial crisis, financial services regulators in the U.S. and internationally revisited their regulatory capital frameworks to address lessons learned. The international efforts of the leading banking regulators through the BCBS culminated in 2010 in enhancements to the Basel framework.[29] That comprehensive reform package was designed to improve the quality and quantity of regulatory capital and to build additional capacity into the banking system to absorb losses during future periods of financial stress. Revisions to the international capital standards included a more restrictive definition of regulatory capital, higher regulatory capital requirements, a capital conservation buffer that could be drawn down during periods of financial stress, and also capital surcharges for systemic importance.

With respect to the Enterprises, HERA gave FHFA greater authority to determine capital standards for the Enterprises by removing the Safety and Soundness Act's restrictions on the risk-based capital requirements and by giving FHFA authority to increase leverage ratio requirements above the statutory minimum. Each Enterprise was placed into conservatorship shortly after enactment of HERA, and FHFA suspended the Enterprises' statutory capital classifications and regulatory capital requirements. FHFA, in its capacity as conservator, then began to develop a framework known as the Conservatorship Capital Framework to ensure that each Enterprise assumed appropriate regulatory capital requirements in managing their businesses. The Conservatorship Capital Framework was implemented in 2017, and ultimately was the foundation of the 2018 proposal.

IV. Rationale for Re-Proposal

FHFA is re-proposing the regulatory capital framework for the Enterprises for three key reasons:

- First, FHFA has begun the process to responsibly end the conservatorships of the Enterprises. This policy change is a departure from the expectations of interested parties at the time of the 2018 proposal, when the prospects for indefinite conservatorships informed comments and perhaps even the decision whether to comment at all.

- Second, FHFA is proposing to increase the quantity and quality of the regulatory capital at the Enterprises to ensure the safety and soundness of each Enterprise and that each Enterprise can fulfill its statutory mission to provide stability and ongoing assistance to the secondary mortgage market across the economic cycle, in particular during periods of financial stress.

- Third, to facilitate regulatory capital planning and also in furtherance of the safety and soundness of the Enterprises and their countercyclical mission, FHFA is proposing changes to mitigate the pro-cyclicality of the aggregate risk-based capital requirements of the 2018 proposal.

While these enhancements preserve the 2018 proposal as the foundation of the Enterprises' regulatory capital framework, FHFA has nonetheless determined to solicit comments on this revised framework in its entirety in light of the changed policy environment, the extent and nature of the enhancements, the technical nature of the underlying issues, the diverse range of interested parties, and the critical importance of the Enterprises' regulatory capital framework to the national housing finance markets.

A. Responsibly Ending the Conservatorships

FHFA stated in the 2018 proposal that “this proposed rule is not a step towards recapitalizing the Enterprises and administratively releasing them from conservatorship.” [30] FHFA also noted that “[p]ublication of this proposed rule will assist with FHFA's administration of the conservatorships of Fannie Mae and Freddie Mac by potentially refining the [Conservatorship Capital Framework].” [31] It is possible that these and other statements made by FHFA, as well as the generally prevailing uncertainty at the time as to the Enterprises' prospects for exiting conservatorships, might have influenced interested parties' views as to the practical relevance of the 2018 proposal or otherwise dissuaded the submission of some comments. In fact, more than half of the comments on the 2018 proposal related to the ongoing conservatorships rather than the proposed regulatory capital framework.

The policy environment has since changed. In September 2019, the Treasury Department released its housing reform plan that recommended that FHFA begin the process to end each Enterprise's conservatorship in a manner consistent with the preconditions set forth in that plan, and also recommended a recapitalization plan be developed for each Enterprise.[32] Shortly thereafter, the Treasury Department and FHFA, on behalf of each Enterprise in its capacity as conservator, entered into letter agreements permitting the Enterprises to together retain up to $45 billion in capital. In October 2019, FHFA then issued a new Strategic Plan and Scorecard for the Enterprises that stated that “[e]nding the conservatorships of Fannie Mae and Freddie Mac is a central and necessary element of this new roadmap.”

These developments were important factors in FHFA's decision to re-propose the regulatory capital framework in its entirety. FHFA considered extensively the comments received on the 2018 proposal and made significant adjustments to multiple aspects of the proposed regulatory capital framework in response to the comments received. FHFA now hopes and expects that the clarity as to the Enterprises' eventual exit from conservatorship will lead to new, different, and more extensive comments. To that end, FHFA emphasizes that the purpose of the proposed rule is to establish a regulatory capital framework that ensures the safety and soundness of each Enterprise and that each Enterprise is positioned to fulfill its statutory mission across the economic cycle, in particular during periods of financial stress.

B. Ensuring Capital Adequacy

1. Quality of Capital

As discussed in Section III.B.3, a lesson of the 2008 financial crisis is that the Enterprises' safety and soundness depends not only on the quantity but also on the quality of their regulatory capital. In light of the lessons learned, FHFA has determined enhancements are necessary to address two key concerns with respect to the quality of the Enterprise's regulatory capital.

First, enhancements are necessary to limit the amount of regulatory capital that may consist of certain components of capital such as DTAs that might tend to have less loss-absorbing capacity during a period of financial stress. FHFA noted in the 2018 proposal that the Enterprises' DTAs, which are included in total capital and core capital by statute, “may provide minimal to no loss-absorbing capability during a period of [financial] stress as recoverability (via taxable income) may become uncertain.” [33] The 2018 proposal addressed this issue by establishing a risk-based capital requirement for DTAs. However, the 2018 proposal did not include adjustments for other capital elements that tend to have less loss-absorbing capacity during a financial stress (e.g., ALLL, goodwill, and intangibles). The 2018 proposal also did not adjust for accumulated other comprehensive income (AOCI), leaving open the possibility that an Enterprise could have positive total capital and core capital despite being insolvent under GAAP, though FHFA did request comment on whether to include offsetting capital requirements to AOCI similar to the treatment of DTAs.

Second, the statutory definitions of regulatory capital used in the 2018 proposal did not limit the extent to which preferred shares could satisfy the risk-based capital requirements. Specifically, there was neither a risk-based capital requirement for core capital nor a requirement that retained earnings and other common equity be the predominant form of capital, as under the Basel framework.[34] The 2018 proposal sought feedback on this issue and commenters recommended FHFA limit the inclusion of preferred shares in regulatory capital to align with the U.S. banking framework's definition of tier 1 capital.

To address these and related concerns, and as described in more detail in Section V.B., FHFA is proposing to supplement the total capital and core capital requirements with additional capital requirements based on the Basel framework's definitions of total capital, tier 1 capital, and CET1 capital. These supplemental capital requirements would include customary deductions and other adjustments for certain DTAs, goodwill, intangibles, and other assets that tend to have less loss-absorbing capacity during a financial stress. The risk-based tier 1 and CET1 capital requirements also would ensure that retained earnings and other high-quality capital are the predominant form of regulatory capital.

2. Quantity of Capital

FHFA has also determined enhancements to the 2018 proposal are necessary to ensure a safe and sound quantity of regulatory capital at each Enterprise. In particular, due in part to the lack of prudential floors on risk-based capital requirements and capital buffers, the 2018 proposal's credit risk capital requirements were insufficient to ensure the safety and soundness of each Enterprise and that each Enterprise could continue to fulfill its statutory mission during a period of financial stress. In determining the need for these enhancements, FHFA considered the following facts, among others:

- Cumulative Crisis-Era Capital Losses. Fannie Mae and Freddie Mac's peak cumulative capital losses from 2008 through 2011 and the first quarter of 2012, respectively, were, respectively, $167 billion and $98 billion. Had the 2018 proposal been in effect at the end of 2007, the 2018 proposal's risk-based capital requirements for Fannie Mae and Freddie Mac would have been, respectively, $171 billion and $110 billion. Fannie Mae and Freddie Mac's peak losses would have left, respectively, only $3 billion and $12 billion in remaining capital. At 0.1 percent and 0.5 percent of their total assets and off-balance sheet guarantees respectively, these amounts would not have sustained the market confidence necessary for the Enterprises to continue as going concerns, particularly given the prevailing stress in the financial markets at that time and also given the uncertainty as to the potential for other write-downs and the adequacy of the Enterprises' allowances for loan losses. Indeed, in October 2010, FHFA projected $90 billion in additional PSPA draws through 2013 under the baseline scenario, although only $34 billion in additional draws proved necessary.[35]

- Single-family Credit Losses. Freddie Mac's estimated single-family credit risk capital requirement under the 2018 proposal of $59 billion as of December 31, 2007 would have been less than its lifetime single-family credit losses of $64 billion on its December 31, 2007 guarantee portfolio. Even excluding loans that Freddie Mac no longer acquires, Freddie Mac's estimated single-family credit risk capital requirement of $24 billion under the 2018 proposal would have exceeded projected lifetime losses of $20 billion by only $4 billion (0.4 percent of the unpaid principal balance on the single-family book as of December 31, 2007). Fannie Mae's estimated single-family credit risk capital requirement under the 2018 proposal would have exceeded projected lifetime losses on its December 31, 2007 guarantee portfolio whether including or excluding loans that it no longer acquires, but only by $9 billion in both scenarios (0.4 percent and 0.7 percent, respectively, of the unpaid principal balance of the single-family book as of December 31, 2007).

- Comparison to the Basel and U.S. Banking Frameworks. Had the 2018 proposal been in effect on September 30, 2019, the average pre-CRT net credit risk capital requirement on the Enterprises' single-family mortgage exposures would have been 1.6 percent of unpaid principal balance, implying an average risk weight of 20 percent.[36] The U.S. banking framework generally assigns a 50 percent risk weight to single-family mortgage exposures to determine the credit risk capital requirement (equivalent to a 4.0 percent adjusted total capital requirement), while the current Basel framework generally assigns a 35 percent risk weight (equivalent to a 2.8 percent adjusted total capital requirement). Before adjusting for the capital buffers under the proposed rule and the Basel and U.S. banking frameworks, the Enterprises' regulatory capital requirements for single-family mortgage exposures under the 2018 proposal would have been 40 percent that of U.S. banking organizations and less than 60 percent that of non-U.S. banking organizations. The BCBS has finalized a more risk-sensitive set of risk weights for residential mortgage exposures, which are to be implemented by January 1, 2022.[37] With those changes, the lowest standardized risk weight would be 20 percent for single-family residential mortgage loans with LTVs at origination less than 50 percent. The 20 percent average risk weight would have been the same as the Basel framework's 20 percent minimum, notwithstanding the Enterprises having an average single-family original loan-to-value (OLTV) of approximately 77 percent as of September 30, 2019. These comparisons are complicated by the fact that the 20 percent average risk weight reflects capital relief for loan-level credit enhancement and MTMLTV. In particular, some meaningful portion of the gap between the credit risk capital requirements of the banking organizations and the Enterprises under the 2018 proposal is due to the 2018 proposal's use of MTMLTV instead of OLTV, as under the U.S. banking framework, to assign credit risk capital requirements for mortgage exposures. In a different house price environment, perhaps after several years of declining house prices, the mark-to-market framework could have resulted in higher credit risk capital requirements than the Basel and U.S. banking frameworks. Similarly, some of this gap might have been expected to narrow had real property prices moved toward their long-term trend. However, the sizing of the current gap under the 2018 proposal is still an important consideration informing the enhancements to the 2018 proposal. Notably, the 20 percent average risk weight would have been the same as the Basel framework's 20 percent risk weight assigned to exposures to sovereigns and central banks with ratings A+ to A− and claims on banks and corporates with ratings AAA to AA−.[38] The 20 percent average risk weight also would have been the same as the 20 percent risk weight assigned under the U.S. banking framework to Enterprise-guaranteed MBS.

- Monoline businesses. As discussed in the 2018 proposal, comparisons to the U.S. banking framework's capital requirements are complicated by the different risk profiles of the Enterprises and large banking organizations.[39] The Enterprises, for example, transfer much of the interest rate and funding risk on their mortgage exposures through their sales of their guaranteed MBS, while large banking organizations generally must fund those loans through customer deposits and other sources. While the interest rate and funding risk profiles are different, that difference should not preclude comparisons of the credit risk capital requirements of the U.S. banking framework to the credit risk capital requirements of the Enterprises. The Basel and U.S. banking frameworks generally do not contemplate an explicit capital requirement for interest rate risk on banking book exposures, leaving interest rate risk capital requirements to bank-specific tailoring through the supervisory process.[40] If anything, the monoline nature of the Enterprises' mortgage-focused businesses actually suggests that the concentration risk of an Enterprise might be greater than that of a diversified banking organization with a similar amount of credit risk. FHFA has not attempted to make a specific adjustment to the risk-based capital requirements to mitigate the Enterprises' concentration risk, but the heightened risk associated with the Enterprises' sector-specific concentration is nonetheless an important consideration in determining the need for the enhancements contemplated by the proposed rule.

More generally, enhancements are necessary to mitigate certain risks and limitations associated with the underlying historical data and models used to calibrate the 2018 proposal's credit risk capital requirements. For example:

- Limitations of crisis-era data. Under the 2018 proposal, the credit risk capital requirement for a mortgage exposure was calibrated to be sufficient to absorb the lifetime unexpected losses incurred on loans of that type experiencing a shock to house prices similar to that observed during the 2008 financial crisis. As discussed in Section III.B, the Enterprises' financial crisis-era losses likely were mitigated to at least some extent by the unprecedented support by the federal government of the housing market and the economy, and also by the declining interest rate environment of the period. There is therefore some risk that the 2018 proposal's risk-based capital requirements, notwithstanding the required going-concern buffer, were not calibrated to ensure each Enterprise would be regarded as a viable going concern following an economic downturn that potentially entails more unexpected losses, whether because there is less or no Federal support of the economy, because there is less or no reduction in interest rates, or because of other causes. For example, post-crisis changes in federal, state, and local loss mitigation and other foreclosure requirements might increase the uncertainty as to loss estimations.

- High-risk loan products. A disproportionate share of the Enterprises' crisis-era credit losses (approximately $108 billion) arose from certain single-family mortgage exposures that are no longer eligible for acquisition by the Enterprises. The calibration of the 2018 proposal's credit risk capital requirements attributed a significant portion of the Enterprises' crisis-era losses to these product characteristics, including “Alt-A,” negative amortization, interest-only, and low or no documentation loans, as well as loans with debt-to-income ratio at origination greater than 50 percent, cash out refinances with total LTV greater than 85 percent, and investor loans with LTV greater than or equal to 90 percent. The statistical methods used to allocate losses between borrower-related risk attributes and product-related risk attributes pose significant model risk. To ensure safety and soundness, the capital requirements should mitigate the risk of potential underestimation of credit losses that would be incurred in an economic downturn with national housing price declines of similar magnitude, even absent those loan types and even assuming a repeat of Federal support of the economy and the declining interest rate environment.[41]

- Gaps in risk coverage. There are some material risks to the Enterprises that were not assigned a risk-based capital requirement under either the 2018 proposal and the proposed rule—for example, risks relating to uninsured or underinsured losses from flooding, earthquakes, or other natural disasters or radiological or biological hazards. There also is no risk-based capital requirement for the risks that climate change could pose to property values in some localities.

Related to these capital adequacy concerns, the 2018 proposal's required capital was not tailored to the risk that a default or other financial distress of an Enterprise could have on the liquidity, efficiency, competitiveness, or resiliency of national housing finance markets. As described in Section VII.A.3, the absence of a stability capital buffer poses not only a risk to the national housing finance markets but also a risk to the safety and soundness of the Enterprises by perpetuating their funding advantages and undermining market discipline over their risk taking.

To address these and related concerns, and as described in more detail below, FHFA is proposing, among other changes:

- A prudential floor on the credit risk capital requirement for mortgage exposures to mitigate the model and other risks associated with the methodology for calibrating the credit risk capital requirements.

- A credit risk capital requirement on senior tranches of CRT held by an Enterprise, an adjustment to the CRT capital treatment to reflect that CRT is not equivalent in loss-absorbing capacity to equity financing, and operational criteria for CRT structures that together would mitigate the structuring, recourse, and other risks associated with these securitizations.

- Risk-based capital requirements for a number of exposures not expressly addressed by the 2018 proposal, including credit risk on commitments to acquire mortgage loans, counterparty risk on interest rate and other derivatives, and credit risk on an Enterprise's holdings or guarantees of the other Enterprise's MBS.

- A countercyclical adjustment for single-family credit risk that would result in greater capital retention when housing markets may be vulnerable to correction, while better enabling the Enterprises to play a countercyclical role.

- A stress capital buffer that would, among other things, enhance the resiliency of the Enterprises and ensure that each Enterprise would continue to be regarded as a viable going concern by creditors and other counterparties after a severe economic downturn.

- A stability capital buffer tailored to the risk that the Enterprise's default or other financial distress could have on the liquidity, efficiency, competitiveness, and resiliency of national housing finance markets.

- A revised method for determining operational risk capital requirements, as well as a higher floor.

- A requirement that each Enterprise maintain internal models for determining its own risk-based capital requirements that would prompt each Enterprise to develop its own view of credit and other risks and not rely solely on the risk assessments underlying the standardized risk weights assigned under this regulatory capital framework.

- A 2.5 percent leverage ratio and a 1.5 percent PLBA that would together serve as a credible backstop to the risk-based capital requirements and mitigate the inherent risks and limitations of any methodology for calibrating those requirements.

C. Addressing Pro-Cyclicality

Consistent with many of the comments on the 2018 proposal, FHFA has determined that mitigating the pro-cyclicality of the 2018 proposal's risk-based capital requirements would facilitate capital management, enhance the safety and soundness of the Enterprises by preventing risk-based capital requirements from decreasing to unsafe and unsound levels, and help position the Enterprises to fulfill their statutory mission to provide stability and ongoing assistance to the national housing finance markets across the economic cycle. A pro-cyclical framework could have incentivized the Enterprises to expand credit when house prices increased, potentially left the Enterprises without regulatory capital that could be drawn down during a period of financial stress, and perhaps even exacerbated the housing price cycle itself. A pro-cyclical framework also could have led to large swings in required capital, leading to the practical necessity that prudent management would maintain a managerial capital surplus well above the capital requirements.

As described in more detail below, FHFA is proposing several enhancements to address this pro-cyclicality while preserving the mortgage risk-sensitive framework of the 2018 proposal. Among other changes, FHFA is proposing:

- A countercyclical adjustment to adjust each single-family mortgage exposure MTMLTV when national housing prices are 5.0 percent above or below the inflation-adjusted long-term trend.

- A stress capital buffer and a separate leverage buffer that will, in addition to enhancing the resiliency of the Enterprises, dampen pro-cyclicality by encouraging each Enterprise to retain capital during good times while remaining able to provide stability and ongoing assistance to the secondary mortgage market during a period of financial stress by utilizing capital buffers as losses are experienced.

- A prudential floor on the credit risk capital requirement for mortgage exposures that, in addition to mitigating the model and other risks associated with the methodology for calibrating the credit risk capital requirements, would also provide further stability to the risk-based capital requirements through the cycle.

- A requirement that each Enterprise maintain its own view of credit and other risks, including as to the relationship between housing prices and market fundamentals, by maintaining its own internal models for determining risk-based capital.

V. Definitions of Regulatory Capital

A. Statutory Definitions

As discussed in Sections VI.A and VI.B, the proposed rule would require each Enterprise to maintain required amounts of core capital and total capital, as defined in the Safety and Soundness Act.

Core capital means, with respect to an Enterprise, the sum of the following (as determined in accordance with GAAP):

- The par or stated value of outstanding common stock;

- The par or stated value of outstanding perpetual, noncumulative preferred stock;

- Paid-in capital; and

- Retained earnings.

Core capital does not include any amounts that the Enterprise could be required to pay, at the option of investors, to retire capital instruments.

Total capital means, with respect to an Enterprise, the sum of the following:

- The core capital of the Enterprise;

- A general allowance for foreclosure losses, which: (i) Includes an allowance for portfolio mortgage losses, an allowance for non-reimbursable foreclosure costs on government claims, and an allowance for liabilities reflected on the balance sheet for the Enterprise for estimated foreclosure losses on mortgage-backed securities; and (ii) does not include any reserves of the Enterprise made or held against specific assets; and

- Any other amounts from sources of funds available to absorb losses incurred by the Enterprise, that the Director by regulation determines are appropriate to include in determining total capital.

Notably, as discussed in Section IV.B.1, these statutory definitions do not include deductions and other adjustments for capital elements that might tend to have less loss-absorbing capacity during a period of financial stress (e.g., DTAs, ALLL, goodwill, and intangibles). These statutory definitions also do not limit the extent to which preferred shares may satisfy the risk-based capital requirements.

B. Supplemental Definitions

1. Loss-Absorbing Capacity

Following HERA's amendments to the Safety and Soundness Act, FHFA has wide authority to prescribe regulatory capital requirements for the Enterprises. The Safety and Soundness Act generally authorizes FHFA to prescribe by regulation risk-based capital requirements for the Enterprises.[42] The Safety and Soundness Act also authorizes FHFA to prescribe minimum capital levels that are greater than the levels prescribed by statute.[43] The FHFA Director has general regulatory authority over the Enterprises, as well as the authority to issue regulations to carry out the duties of the FHFA Director.[44] The FHFA Director also may establish such other operational and management standards as the FHFA Director determines to be appropriate.[45] As amended by HERA, these and other provisions of the Safety and Soundness Act give the FHFA Director generally broad and flexible authority to tailor regulatory capital requirements for the Enterprises, including to prescribe additional capital requirements that supplement the statutory capital classifications based on total capital and core capital.

FHFA is proposing to supplement the statutory definitions of total capital and core capital requirements with additional regulatory capital definitions based on the Basel framework's definitions of total capital, tier 1 capital, and CET1 capital. These supplemental definitions would include customary deductions and other adjustments for certain DTAs, goodwill, intangibles, and other assets that tend to have less loss-absorbing capacity during a financial stress. As discussed in Section IV.B.1, the supplemental definitions of regulatory capital would fill certain gaps in the statutory definitions of core capital and total capital. For example, neither core capital nor total capital adjust for AOCI, leaving open the possibility that an Enterprise could have positive total capital and core capital but yet be insolvent under GAAP. The supplemental tier 1 and CET1 capital requirements also would ensure that retained earnings and other high-quality capital are the predominant form of regulatory capital.