AGENCY:

Federal Deposit Insurance Corporation.

ACTION:

Advance notice of proposed rulemaking and request for comment.

SUMMARY:

The Federal Deposit Insurance Corporation (FDIC) is undertaking a comprehensive review of the regulatory approach to brokered deposits and the interest rate caps applicable to banks that are less than well capitalized. Since the statutory brokered deposit restrictions were put in place in 1989, and amended in 1991, the financial services industry has seen significant changes in technology, business models, and products. In addition, changes to the economic environment have raised a number of issues relating to the interest rate restrictions. A key part of the FDIC's review is to seek public comment through this Advance Notice of Proposed Rulemaking (ANPR) on the impact of these changes. The FDIC will carefully consider comments received in response to this ANPR in determining what actions may be warranted.

DATES:

Comments must be received by the FDIC no later than May 7, 2019.

ADDRESSES:

You may submit comments on the notice of proposed rulemaking using any of the following methods:

- Agency Website: http://www.fdic.gov/regulations/laws/federal/. Follow the instructions for submitting comments on the agency website.

- Email: comments@fdic.gov. Include RIN 3064-AE94 on the subject line of the message.

- Mail: Robert E. Feldman, Executive Secretary, Attention: Comments, Federal Deposit Insurance Corporation, 550 17th Street NW, Washington, DC 20429.

- Hand Delivery: Comments may be hand delivered to the guard station at the rear of the 550 17th Street NW Building (located on F Street) on business days between 7 a.m. and 5 p.m.

- Public Inspection: All comments received, including any personal information provided, will be posted generally without change to http://www.fdic.gov/regulations/laws/federal.

FOR FURTHER INFORMATION CONTACT:

Legal Division—Thomas Hearn, Counsel, (202) 898-6967; thohearn@fdic.gov; Vivek V. Khare, Counsel, (202) 898-6847, vkhare@fdic.gov; Division of Risk Management Supervision—Thomas F. Lyons, Chief, Policy and Program Development, (202) 898-6850, tlyons@fdic.gov; Judy Gross, Senior Policy Analyst, (202) 898-7047, jugross@fdic.gov; Division of Insurance and Research—Ashley Mihalik, Chief, Banking and Regulatory Policy, (202) 898-3793, amihalik@fdic.gov.

SUPPLEMENTARY INFORMATION:

I. Policy Objectives

The policy objective of this ANPR is to obtain input from the public as the FDIC comprehensively reviews its brokered deposit and interest rate regulations in light of significant changes in technology, business models, the economic environment, and products since the regulations were adopted. The FDIC is inviting comment on all aspects of the brokered deposit and interest rate regulations.

To facilitate comment, the remainder of this ANPR has been structured in the following manner: (II) Brokered Deposits and Interest Rate Restrictions, addressing (A) Current Law and Regulations, (B) History and Research, (C) Brokered Deposit Issues, (D) Interest Rate Issues; (III) Requests for Comment; and Appendices with additional background and descriptive statistics.

II. Brokered Deposits and Interest Rate Restrictions

Brokered and high-rate deposits became a concern among bank regulators and Congress before any statutory restrictions were put in place. This concern arose because: (1) Such deposits could facilitate a bank's rapid growth in risky assets without adequate controls; (2) once problems arose, a problem bank could use such deposits to fund additional risky assets to attempt to “grow out” of its problems, a strategy that ultimately increased the losses to the deposit insurance fund when the institution failed; and (3) brokered and high-rate deposits were sometimes volatile because deposit brokers (on behalf of customers), or the customers themselves, were often drawn to high rates and were prone to leave the bank when they found a better rate or they became aware of problems at the bank.

Before proceeding further, it should be noted that, historically, most institutions that use brokered and higher-rate deposits have done so in a prudent manner and appropriately measure, monitor, and control risks associated with brokered deposits. Moreover, well-capitalized institutions are not subject to restrictions on accepting brokered deposits or setting interest rates. Nonetheless, the FDIC also recognizes that institutions sometimes are concerned that the use of brokered deposits can have other regulatory consequences, such as implications for deposit insurance pricing in certain circumstances, or may be viewed negatively by investors or other stakeholders.

A. Current Law and Regulations

Section 29 of the Federal Deposit Insurance Act (FDI Act), titled “Brokered Deposits,” was originally added to the FDI Act by the Financial Institutions Reform, Recovery, and Enforcement Act of 1989 (FIRREA). The law originally restricted troubled institutions (not meeting their minimum capital requirements at the time) from (1) accepting deposits from a deposit broker without a waiver and (2) soliciting deposits by offering rates of interest on deposits that were significantly higher than the prevailing rates of interest on deposits offered by other insured depository institutions (or “IDIs”) having the same type of charter in such depository institution's normal market area.[1]

Two years later, Congress enacted the Federal Deposit Insurance Corporation Improvement Act of 1991 (FDICIA), which added the Prompt Corrective Action (PCA) capital regime to the FDI Act and also amended the threshold for the brokered deposit and interest rate restrictions from a troubled institution to a bank falling below the “well capitalized” PCA level. At the same time, the FDIC was authorized to waive the brokered deposit restrictions for a bank that is adequately capitalized upon a finding that the acceptance of such deposits does not constitute an unsafe or unsound practice with respect to the institution.[2] FDICIA did not authorize the FDIC to waive the brokered deposit restrictions for less than adequately capitalized institutions. Most recently, earlier this year, Section 29 of the FDI Act was amended as part of the Economic Growth, Regulatory Relief, and Consumer Protection Act, to except a capped amount of certain reciprocal deposits from treatment as brokered deposits.[3]

Section 337.6 of the FDIC's Rules and Regulations implements and closely tracks the statutory text of Section 29, particularly with respect to the definition of “deposit broker” and its exceptions.[4] Section 29 of the FDI Act does not directly define a “brokered deposit,” rather, it defines a “deposit broker” for purposes of the restrictions.[5] Thus, the meaning of the term “brokered deposit” turns upon the definition of “deposit broker.”

Section 29 and the FDIC's implementing regulation define the term “deposit broker” to include:

(1) Any person engaged in the business of placing deposits, or facilitating the placement of deposits, of third parties with insured depository institutions or the business of placing deposits with insured depository institutions for the purpose of selling interests in those deposits to third parties; and

(2) An agent or trustee who establishes a deposit account to facilitate a business arrangement with an insured depository institution to use the proceeds of the account to fund a prearranged loan.

This definition is subject to the following nine statutory exceptions:

(1) An insured depository institution, with respect to funds placed with that depository institution;

(2) An employee of an insured depository institution, with respect to funds placed with the employing depository institution; [6]

(3) A trust department of an insured depository institution, if the trust in question has not been established for the primary purpose of placing funds with insured depository institutions;

(4) The trustee of a pension or other employee benefit plan, with respect to funds of the plan;

(5) A person acting as a plan administrator or an investment adviser in connection with a pension plan or other employee benefit plan provided that that person is performing managerial functions with respect to the plan;

(6) The trustee of a testamentary account;

(7) The trustee of an irrevocable trust (other than one described in paragraph (1)(B)), as long as the trust in question has not been established for the primary purpose of placing funds with insured depository institutions;

(8) A trustee or custodian of a pension or profit sharing plan qualified under section 401(d) or 430(a) of the Internal Revenue Code of 1986; or

(9) An agent or nominee whose primary purpose is not the placement of funds with depository institutions.

As listed above, the statute includes nine exceptions to the definition of “deposit broker.” The FDIC's regulations include the following tenth exception: “An insured depository institution acting as an intermediary or agent of a U.S. government department or agency for a government sponsored minority or women-owned depository institution program (“MWODI”).[7]

In addition to restricting the acceptance of brokered deposits by less than well-capitalized IDIs, Section 29 of the FDI Act also prohibits such IDIs from paying rates that significantly exceed their normal market area or the national rate as established by the FDIC by regulation. This provision was intended to prohibit “the solicitation of deposits by in-house salaried employees through so-called money-desk operations.” [8] More specifically, the provision addressed a concern that emerged during various legislative hearings that brokered deposit restrictions could easily be circumvented by in-house solicitation of high-rates.[9] In implementing this legislative restriction, from 1989 to 2009, the FDIC pegged the national rate to comparable Treasury rates in its regulation. However, the national rate calculation was changed in 2009, pursuant to a notice-and-comment rulemaking, when yields on Treasuries fell dramatically during the crisis, compressing the rate caps. The FDIC moved to a simple average of rates paid by all banks and branches that offer a specific product. This national rate data is provided to the FDIC by a data-gathering company and is published weekly on the FDIC's website. The history of the interest rate restrictions and its associated issues are discussed more fully in Section D.

B. History and Research

As described in the FDIC's 1997 study of the banking and thrift crises of the 1980s and early 1990s, brokered CDs became increasingly used as funding sources, first by money center banks and then by regional and smaller institutions.[10] Even as early as the 1970s, the FDIC noted concerns about brokered deposits, as stated in the FDIC's Division of Bank Supervision Manual—“The use of brokered deposits has been responsible for abuses in banking and has contributed to some bank failures, with consequent losses to the larger depositors, other creditors, and shareholders.” [11]

However, the potential abuses associated with brokered deposits received relatively little attention until the failure of Penn Square Bank in 1982. This failure resulted in the largest bank payout of insured deposits in the history of the FDIC up until that time.[12] Brokered deposits allowed the bank to grow rapidly from $30 million in assets in 1977 to $436 million in assets when it failed in 1982, with much of the growth in high risk loans to small oil and gas producers.[13] In response to the rising use of brokered deposits and data suggesting negative consequences, in April 1984 the FDIC and the Federal Home Loan Bank Board (FHLBB) adopted a joint final rule restricting pass through deposit insurance for deposits obtained through a deposit broker.[14] The agencies indicated that data showed that institutions used brokered deposits to pursue rapid growth in risky real estate-related lending without adequate controls and to increase risky lending after problems arose. In January 1985, the Court of Appeals for the District of Columbia Circuit ruled that the FDI Act did not permit the FDIC to eliminate pass-through deposit insurance for deposit brokers.[15]

While the case was pending, and after the decision, Congressional hearings regarding brokered deposits were held between 1984 and 1988 and, in 1989, as noted earlier, as part of FIRREA. Pursuant to these hearings, Congress imposed restrictions on brokered deposits for institutions that did not meet their minimum capital requirements and later tied the restrictions to the PCA framework in 1991 through FDICIA. Congress also imposed rate restrictions on institutions that were less than well capitalized out of concern that institutions would be able to circumvent brokered deposit restrictions by merely advertising or otherwise offering very high rates. Since enactment of Section 29, the FDIC has continued to study the role of brokered deposits in the performance of banks, their impact on safety and soundness, and the loss they impose on the Deposit Insurance Fund (DIF) when a bank fails.

Brokered Deposit Usage and Relevant Data

From the 1960s up until 2000, brokered retail CDs and wholesale CDs were the main type of brokered deposits used in the banking system. Starting in the 1980s deposit listing services began generating deposits for IDIs by advertising CD rates on behalf of institutions. Beginning in 1999, broker-dealers first started to offer brokerage customers an automatic sweep of their customers' idle funds to IDIs.

Beginning in 2003, a network was established through which banks could place customer funds in time deposits at other banks and receive time deposits in an equal amount of funds in return, such deposits being referred to as “reciprocal deposits.” Similar services evolved for money market deposit accounts (MMDAs).

As of September 30, 2018, insured depository institutions held $986 billion in brokered deposits, which amounted to 8.0 percent of the $12.3 trillion in industry domestic deposits. These brokered deposits were held by 2,221 insured depository institutions, representing 40.6 percent of the 5,477 total number of insured depository institutions.

Although 2,221 institutions held brokered deposits as of September 30, 2018, a significant portion of these deposits are concentrated in a small number of institutions. One hundred institutions held 89.4 percent, or $881 billion, of the $986 billion brokered deposits in the banking system, with five institutions accounting for 39.4 percent, or $389 billion, of all brokered deposits. The remaining 2,121 institutions using brokered deposits account for the remaining $104 billion in brokered deposits.

Consistent with this concentration, among the 2,221 institutions holding brokered deposits as of September 30, 2018, the median holding was 4.7 percent of total domestic deposits, but 6 institutions held brokered deposits in excess of 90 percent of total domestic deposits; 25 institutions held brokered deposits between 50 percent and 90 percent of total domestic deposits; and 79 institutions held brokered deposits between 25 percent and 50 percent of total domestic deposits.

| Asset size group | Total number of banks | Number of banks with brokered deposits | Total brokered deposits (billions) | Share of total brokered deposits (%) | Total domestic deposits | Share of total domestic deposits (%) |

|---|---|---|---|---|---|---|

| Under $1 Billion | 4,704 | 1,656 | $31.92 | 3.2 | $988.05 | 8.0 |

| $1-10 Billion | 635 | 439 | 90.16 | 9.1 | 1,349.56 | 11.0 |

| $10-50 Billion | 97 | 89 | 171.87 | 17.4 | 1,605.40 | 13.0 |

| Over $50 Billion | 41 | 37 | 691.78 | 70.2 | 8,378.84 | 68.0 |

| All Banks | 5,477 | 2,221 | 985.73 | 12,321.84 |

The largest concentrations of brokered deposits can be characterized as 3 types of deposits: (1) Master Certificates of Deposits; (2) sweep deposits that are viewed as brokered; and (3) reciprocal deposits. Listing service deposits are also discussed below, but typically, are not reported as brokered.

Master Certificate of Deposits

Information about brokered deposits that the FDIC collects from banks through the Call Report does not reflect certain elements of the structure of the brokered deposit market. However, industry participants have informed the FDIC that a sizable portion of reported brokered deposits are wholesale Master Certificate of Deposits. These instruments are held on the books of the issuing bank in the name of a subsidiary of Depository Trust Corporation (DTC) as custodian for deposit brokers who are often broker dealers. These broker dealers, in turn, issue retail CDs, typically in denominations of $1,000, under the Master Certificate of Deposit to their retail clients.

The retail customers' ownership interests in the brokered retail CDs are reflected on the books of the deposit broker that issued them. These Master Certificates of Deposits are reported by banks on Call Report Schedule RC-E, Memoranda Item 1.c as deposits of $250,000 or less even though issued in the name of DTC for more than $250,000 to reflect the substance of the retail CDs issued under them. The FDIC, however, has no Call Report information about what portion of reported brokered deposits of $250,000 or less are Master Certificates of Deposits as described above. In the event of a failure, the deposit broker maintains records of the retail CDs held by its customers, and these records would be submitted to the FDIC in order to make payments on deposit insurance to the retail CD holders.

Sweep Deposits

Third parties (including investment companies acting on behalf their clients) that sweep client funds into deposit accounts at IDIs are deposit brokers. As a result, the sweep deposits placed by these third parties are brokered deposits unless the third party meets one of the exceptions to the definition of “deposit broker”. In 2005, FDIC staff issued an advisory opinion that took the view that a brokerage firm placing idle client funds into deposit accounts at its affiliate IDI, under certain circumstances, meets the “primary purpose” exception.[17] Thus, the deposits placed on behalf of their clients would not be brokered deposits.

As of September 30, 2018, 28 insured depository institutions have indicated to the FDIC that they receive funds swept from an affiliated broker dealer under conditions that FDIC staff have indicated would support the affiliate being viewed as meeting the “primary purpose” exception to the “deposit broker” definition. Each of these insured depository institutions provides monthly reports to the FDIC of the monthly average of the swept funds as of month end. As of September 30, 2018, these 28 insured depository institutions reported $724 billion as the average amount of funds swept from the institutions' affiliated broker dealers for September 2018.

Thus, as of September 30, 2018, the reported brokered deposits of $986 billion, which includes brokered CDs and broker dealer sweeps to unaffiliated insured depository institutions, when combined with the average monthly balance of funds that broker dealers sweep to affiliated institutions for September of $724 billion result in a combined amount of $1.710 trillion, which represents 14 percent of the $12.3 trillion in industry domestic deposits for that date.

Reciprocal Deposits

Reciprocal deposit arrangements are based upon a network of IDIs that place funds at other participating banks in order for depositors to receive insurance coverage for the entire amount of their deposits. Because reciprocal arrangements can be complex, and involve numerous banks, they are often managed by a third-party sponsor. As a result, all deposits placed through this arrangement have historically been viewed as brokered deposits.

On May 24, 2018, the Economic Growth, Regulatory Reform, and Consumer Protection Act took effect, allowing certain banks to except a limited amount of reciprocal deposits (as defined by the Act) from brokered deposits. Under the reciprocal deposit exception, well-capitalized and well-rated institutions are not required to treat such reciprocal deposits as brokered deposits up to the lesser of 20 percent of its total liabilities, or $5 billion. Institutions that are not both well capitalized and well rated may also exclude reciprocal deposits from their brokered deposits under certain circumstances.

The immediate result of this Act has significantly reduced the percentage of reciprocal deposits that are classified as brokered deposits. As of March 30, 2018, the last reporting quarter before the Act took effect, reciprocal deposits of $48.5 billion were reported. As of June 30, 2018, the first quarter end after the Act took effect, brokered reciprocal deposits had fallen to $17.1 billion. As of September 30, 2018, brokered reciprocal deposits had fallen to $13.7 billion. For banks with assets less than $1 billion, their percentage of reciprocal deposits as a percent of brokered deposits declined from 33.7 percent on March 31, 2018, to 15.4 percent on June 30, 2018 and, 11.5 percent on September 30, 2018.

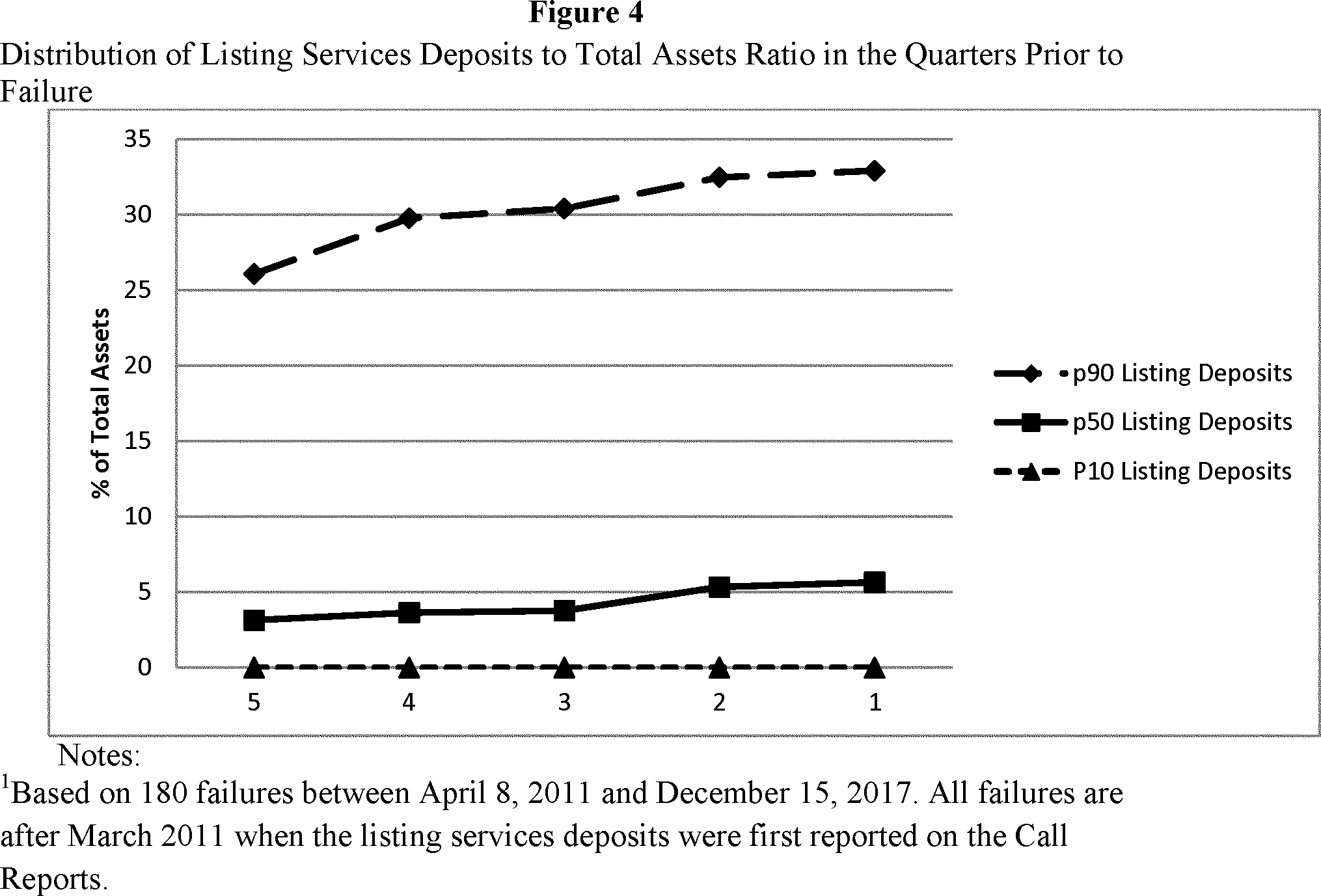

Listing Service Deposits

Deposits whose placement at insured depository institutions are facilitated, in a passive manner, by deposit listing services have not been reported as brokered deposits. However, since 2011, such deposits have been reported on banks' Call Reports. As of September 30, 2018, insured depository institutions reported holding $69.6 billion in listing service deposits that are not reported as brokered deposits, which amounted to 0.6 percent of industry domestic deposits. One quarter of insured depository institutions held non-brokered listing service deposits as of September 30, 2018.

As of September 30, 2018, 22 institutions were not well capitalized for PCA purposes. Of these institutions, 13 institutions held non-brokered listing service deposits, for which the ratio of non-brokered listing service deposits to domestic deposits was 3.6 percent, while the ratio for the 1,356 well-rated institutions holding such deposits was 2.9 percent. Among insured depository institutions with non-brokered listing service deposits, the share of non-brokered listing service deposits to domestic deposits has declined from a median of 4.6 percent on September 30, 2011 to 2.9 percent as of September 30, 2018.

FDIC Studies That Discuss Brokered Deposits

In the wake of the recent financial crisis, the Dodd-Frank Act directed the FDIC to conduct a study of core and brokered deposits, which the FDIC completed in July 2011. Recently the FDIC updated its analysis with data through the end of 2017. The results of that analysis confirm the previous findings of the 2011 study and can be found in Appendix 2.

The research provided in the study shows that higher brokered deposit use is associated with higher probability of bank failure and higher insurance fund loss rates. Banks with higher levels of brokered deposits are also, in general, more costly to the DIF when they fail. The study also found that, on average, brokered deposits are correlated with higher levels of asset growth, higher levels of nonperforming loans, and a lower proportion of core deposit funding. FDIC's study also describes the three characteristics of brokered deposits that have posed risk to the DIF:

1. Rapid growth—the extent to which deposits can be gathered quickly and used imprudently to expand risky assets or investments.

2. Volatility—the extent to which deposits might flee if the institution becomes troubled or the customer finds a more appealing interest rate or terms elsewhere. Volatility tends to be also be mitigated somewhat by deposit insurance, as insured depositors have less incentive to flee a problem situation.

3. Franchise Value—the extent to which deposits will be attractive to the purchasers of failed banks, and therefore not contribute to losses to the DIF.

In December 2017, the FDIC published Crisis and Response: An FDIC History, 2008-2013.[18] The history shows that failures and downgrades were highly correlated with reliance on brokered deposits and other wholesale funding sources.[19] Generally speaking, failures were more concentrated among banks that made relatively greater use of brokered deposits and other wholesale funding sources.

The history noted that, although the use of brokered deposits and other wholesale funding sources within a sound liquidity management program is not in itself a risky practice, significant reliance on wholesale funds may reflect a decision that an institution has made to grow its business more aggressively. On the liability side, the history indicated that if the institution comes under stress, wholesale counterparties may be more apt to withdraw funding or demand additional collateral.

In addition to these publications, the following reports prepared by the Inspectors General of the federal banking agencies have detailed how brokered deposits were sometimes used by failed banks in the most recent crisis. These reports include the following:

- Safety and Soundness: Analysis of Bank Failures Reviewed by the Department of the Treasury Office of Inspector General, OIG-16-052, August 15, 2016

- Summary Analysis of Failed Bank Reviews, Board of Governors of the Federal Reserve System, Office of Inspector General, September 2011

- Follow Up Audit of FDIC Supervision Program Enhancements, FDIC Office of Inspector General, Report No. MLR-11-010, December 2011

In these reports, brokered deposits were most commonly cited as a contributor to problems at troubled and failed institutions, largely by allowing institutions with concentrations in poorly underwritten and administered commercial real estate loans, including acquisition, construction, and development loans (ADC) or other risky assets, to grow rapidly. Institutions that failed were typically subject to the brokered deposit restrictions and interest rate restrictions before failure because their capital levels deteriorated to below well capitalized. However, for those institutions that failed and still had brokered deposits at the time of failure, either the acquirer did not want the brokered deposits or did not pay a premium for them, either of which increases the cost to the DIF.

Brokered Deposits in Bank Failures 2007-2017

The FDIC and the DIF were significantly affected by the previous financial crisis between 2007 and 2017. During this time, excluding Washington Mutual, 530 banks failed and were placed in FDIC receivership and, as of December 31, 2017, the estimated loss to the DIF for these institutions is $74.4 billion.

Based upon regulatory reporting data, 47 institutions that failed relied heavily on brokered deposits and caused losses to the DIF that triggered material loss reviews. These 47 institutions held total assets representing 13 percent of the $703.9 billion in aggregate total assets of the 530 failed institutions, but accounted for $28.4 billion in estimated losses to the DIF, representing 38 percent of the $74.4 billion in all DIF estimated losses for that same period.[20]

For example, the largest of these 47 institutions was IndyMac Bank, F.S.B., which failed on July 11, 2008. As of December 31, 2017, the estimated loss to the DIF for IndyMac, is $12.3 billion, representing 40 percent of IndyMac's $30.7 billion in total assets at failure and approximately 16.5 percent of the total $74.4 billion in estimated losses to the DIF from bank failures between 2007 and 2017. In its last Thrift Financial Report (“TFR”) filed prior to failure, as of March 30, 2008, IndyMac reported brokered deposits of $5.5 billion, which represented 28.98 percent of the institution's $18.9 billion in total deposits.[21] In its TFR filed for the 4th quarter of 2005, approximately 12 quarters before the institution failed, IndyMac reported $1.4 billion in brokered deposits, representing 18.4 percent of its then $7.4 billion in total deposits. This data suggests that IndyMac accelerated its use of brokered deposits as its problems mounted.[22]

Another, more pronounced, example is ANB Financial National Association (ANB Financial), which failed on May 9, 2008. As of November 26, 2018, the estimated loss to the DIF for ANB Financial is $1.029 billion, representing 54 percent of the institution's $1.89 billion in total assets at failure. In its Call Report filed prior to failure, i.e., as of March 30, 2008, ANB Financial reported brokered deposits of $1.578 billion, which represented 86.96 percent of the institution's $1.815 billion in total deposits. In the Call Report filed for the 4th quarter of 2005, approximately 12 quarters before the institution failed, ANB Financial reported $256.8 million in brokered deposits, representing 50.46 percent of its then $508 million in total deposits.[23] The brokered deposits remaining at failure for both IndyMac and ANB's brokered deposits were master CDs issued in the name of DTC as sub-custodian for deposit brokers, which were the primary source for the remaining brokered deposits at failure for most of the other 34 institutions referenced above.

Brokered Deposits and Assessments

The FDIC has amended its assessment regulations to address the risks to the DIF associated with brokered deposits. For small banks (generally, IDIs with less than $10 billion in total assets), brokered deposits can increase a bank's assessment rate if the bank's ratio of brokered deposits to total assets exceeds 10 percent.[24] The brokered deposit ratio is one of several financial measures used to determine assessment rates for small banks. For new small banks in Risk Categories II, III and IV, and large and highly complex institutions that are not well capitalized, or that are not CAMELS composite 1- or 2-rated, brokered deposits can increase a bank's assessment rate through the brokered deposit adjustment.[25] Under the adjustment, a bank's assessment will increase if its ratio of brokered deposits to domestic deposits is greater than 10 percent.

C. Brokered Deposit Issues

As noted above, Section 29 does not explicitly define the term “brokered deposit.” Restrictions on brokered deposits are tied to the statutory definition of “deposit broker” that Congress adopted in 1989 as part of the legislative response to the bank and thrift crisis. That definition includes dealers in the brokered CD market, and broker dealers that sweep customer funds to unaffiliated insured depository institutions which, when combined, represent over 90% of reported brokered deposits according to industry sources as discussed more fully above. Therefore, based on those same sources, the interpretive issues tend to relate to a small segment of reported brokered deposits.

Determining what constitutes a deposit broker, and thus a brokered deposit, is very fact-specific and requires a close review of the arrangement, the documents governing the arrangement, and the third party's remuneration, among other things. Given the wide, and evolving, variety of third-party arrangements, FDIC staff review them on a case-by-case basis, applying the statutory provisions to the facts and circumstances presented. Staff interpretations are typically documented in Advisory Opinions.[26] In addition, on June 30, 2016, the FDIC issued, after soliciting comment, an updated set of Frequently Asked Questions,[27] that compiles information about the law, regulation, and FDIC staff interpretations in a single online location.

The FDIC continues to receive inquiries, and in recent years, FDIC staff has been asked about the application of the “deposit broker” definition, and its statutory and regulatory exceptions, to new types of third parties that are involved in placing or facilitating the placement of third-party funds at IDIs. Many of these questions relate to advancements in technology, and new business practices and products that IDIs might utilize to offer services to customers and also to gather deposits. The inherent challenge often is to distinguish between third party service providers to the IDI and third parties that are engaged in the business of placing or facilitating the placement of deposits, albeit using updated technology.

Generally, in determining whether deposits placed through these new deposit placement arrangements are brokered, staff has looked to precedents involving the definition of “deposit broker” and has attempted to consistently apply that analysis to these new products. If a third party is placing funds on behalf of itself, the funds are not brokered. If a third party is in the business of either (1) placing funds, or (2) facilitating the placement of funds—of another third-party (such as its customers)—then it meets the definition of “deposit broker” and the deposits are brokered, unless an exception applies.

Below is a discussion of a few of the most typical issues for which questions have arisen, organized in the context of the definitions and exceptions.

The FDI Act defines “deposit broker” to mean:

(A) any person engaged in the business of placing deposits, or facilitating the placement of deposits, of third parties with insured depository institutions or the business of placing deposits with insured depository institutions for the purpose of selling interests in those deposits to third parties; [28] and

(B) an agent or trustee who establishes a deposit account to facilitate a business arrangement with an insured depository institution to use the proceeds of the account to fund a prearranged loan.” [29]

1. Engaged in the Business of Placing Deposits or Facilitating the Placement of Deposits

The first phrase of FDI Act section 29(g)(1)(A), defines a deposit broker as, “any person engaged in the business of placing deposits, or facilitating the placement of deposits, of third parties with insured depository institutions.” [30] In evaluating whether certain third parties comport with the statutory definition of “deposit broker,” and being “engaged in the business of placing deposits, or facilitating the placement of deposits,” staff at the FDIC reviews every arrangement on a case-by-case basis considering the following factors:

○ Whether the third party receives fees from the insured depository institution that are based (in whole or in part) on the amount of deposits or the number of deposit accounts.

○ Whether the fees can be justified as compensation for administrative services (such as recordkeeping) or other work performed by the third party for the insured depository institution (as opposed to compensation for bringing deposits to the insured depository institution).

○ Whether the third party's deposit placement activities, if any, is directed at the general public as opposed to being directed at members (or “affinity groups”) or clients.

○ Whether there is a formal or contractual agreement between the insured depository institution and the third party (e.g., referring or marketing entity) to place or steer deposits to certain insured depository institutions.

○ Whether the third party is given access to the depositor's account, or will continue to be involved in the relationship between the depositor and the insured depository institution.

2. Exclusions From the “Deposit Broker” Definition

The statutory “deposit broker” definition excludes the following:

(A) An insured depository institution, with respect to funds placed with that depository institution;

(B) An employee of an insured depository institution, with respect to funds placed with the employing depository institution;

(C) A trust department of an insured depository institution, if the trust in question has not been established for the primary purpose of placing funds with insured depository institutions;

(D) The trustee of a pension or other employee benefit plan, with respect to funds of the plan;

(E) A person acting as a plan administrator or an investment adviser in connection with a pension plan or other employee benefit plan provided that that person is performing managerial functions with respect to the plan;

(F) The trustee of a testamentary account;

(G) The trustee of an irrevocable trust (other than one described in paragraph (1)(B)), as long as the trust in question has not been established for the primary purpose of placing funds with insured depository institutions;

(H) A trustee or custodian of a pension or profit-sharing plan qualified under section 401(d) or 403(a) of Title 26; or

(I) An agent or nominee whose primary purpose is not the placement of funds with depository institutions.[31]

In 1992, the FDIC incorporated in its regulations the list of statutory exceptions to the “deposit broker” definition and added as an additional exception, “an insured depository institution acting as an intermediary or agent of a U.S. government department or agency for a government sponsored minority or women-owned depository institution.” [32]

(a) IDI Exception

The statute provides an exception for an IDI with respect to funds placed with that IDI. Staff notes that based on the plain language of the statute, staff has consistently applied this exception strictly to the IDI itself and not to separately incorporated legal entities such as subsidiaries or other affiliates. One challenging issue relates to wholly-owned subsidiaries that place deposits under an exclusive relationship with the parent IDI. With regard to wholly-owned subsidiaries, for some purposes the subsidiary is treated as part of the parent IDI (e.g., certain financial reporting); whereas for other purposes—such as under the Bank Merger Act and for receivership purposes—they are treated separately.

(b) Employee Exception

Section 29(g)(2)(B) of the FDI Act provides that “deposit broker” does not include “an employee of an insured depository institution, with respect to funds placed with the employing depository institution” (employee exception). The employee exception recognizes that banks are corporate entities that operate through the natural persons they employ.

To address concerns that the employee exception could be used to evade the deposit broker definition, the term “employee” is defined for purposes of section 29, as any employee:

1. Who is employed exclusively by the insured depository institution;

2. Whose compensation is primarily in the form of a salary;

3. Who does not share such employee's compensation with a deposit broker;

4. Whose office space or place of business is used exclusively for the benefit of the insured depository institution which employs such individual.[33]

Particularly after the passage of the Gramm-Leach-Bliley Act and the permissibility of additional relationships among affiliated entities, FDIC staff has dealt with an increase in questions about IDI employees who also have some form of contractual relationship with a third party, usually an affiliate of the IDI. In addition, FDIC staff has informally addressed questions related to the use of premises that are shared by the IDI and an affiliate.

(c) Pension or Other Employee Benefit Plans

Section 29(g)(2)(D) and (E) exclude from the deposit broker definition, trustees of pension and other employee benefit plans with respect to funds in the plan, and administrators or investment advisors provided that the person is performing managerial functions with respect to the plan.[34] Section 29(g)(2)(H) excludes a trustee or custodian of a pension or profit-sharing plan under sections 401(d) or 403(a) of the Internal Revenue Code.[35]

Individual retirement accounts (IRAs) are retirement accounts set up outside of a pension plan or employee benefit plan and thus are not expressly covered by these exceptions. Certain non-retirement savings plans are also granted tax-favored status under the Internal Revenue Code, such as 529 savings plans for higher education tuition and health savings accounts but are not expressly covered by the exception. If a bank's trust department serves as the trustee or custodian of such plans, and the trust has not been established for the primary purpose of placing funds with IDIs, the plans' deposits would not be treated as brokered deposits because of the exception for trust departments. FDIC staff has received a number of questions about this exception.

(d) Primary Purpose Exception

The primary purpose exception applies to “an agent or nominee whose primary purpose is not the placement of funds with depository institutions.” [36] In particular, the primary purpose exception applies to a third party when that third party is acting as agent/nominee for the depositor. Staff's evaluation of a third party's primary purpose in placing deposits has been in the context of that particular agent/principal relationship.

In interpreting what it means for a third-party agent to act pursuant to a “primary purpose,” staff has generally analyzed whether placing—or facilitating the placement—of deposits of its customers/clients when acting as agent for those customers/clients, is for a substantial purpose other than to provide (1) deposit insurance, or (2) a deposit-placement service. In analyzing this principle, staff has considered whether the deposit-placement activity is incidental to some other purpose.

In determining whether a deposit-placement activity is incidental to some other purpose, staff reviews the reason or intent of the third party when acting as agent or nominee in placing the deposits, as well as other factors which might indicate whether the third party agent is incentivized to place deposits at the IDI. Factors that staff has considered include the existence and structure of fee arrangements and of any programmatic relationship between the third party and the insured depository institution.

- Fees:

○ Whether the entity placing deposits receives fees from the insured depository institution that are based (directly or indirectly) on the amount of deposits or the number of deposit accounts opened.

○ Whether the fees can be justified as compensation for recordkeeping or other work performed by the third party for the IDI (as opposed to compensation for bringing deposits to the IDI).

- Programmatic relationship:

○ Whether there is a formal or contractual agreement between IDIs and the placing/referring entity to place or steer deposits to certain IDIs.

Importantly, when interpreting the applicability of the primary purpose exception, staff analyzes the deposit placement arrangement, including the underlying agreements, between the third party agent, the depositor, and the IDI to determine the primary purpose of the agent. The exception applies to agents or nominees, which by definition, act on behalf of principals. When acting in that capacity, the third party agent/nominee is limited to the principal's goals and objectives. Staff does not solely rely upon the business purpose of the third party involved. Staff has not considered the size of the third party or the amount or percentage of revenue that the deposit-placement activity generates.

Primary Purpose Exception for Affiliated Sweeps

Beginning in 1999, the FDIC became aware of broker dealers offering their brokerage customers an automatic sweep program by which customers' idle funds were swept to affiliated insured depository institutions.

In 2005, the FDIC's General Counsel issued a staff opinion indicating FDIC staff view that, when certain conditions are observed, the primary purpose of a broker dealer in sweeping customer funds into deposit accounts at its affiliated IDI is to facilitate the customers' purchase and sale of securities. Among the conditions are that funds are not swept to a time deposit account and do not exceed 10 percent of the total assets handled by the affiliated broker dealer. The insured depository institution is permitted to pay fees to the affiliated broker dealer but the fees must be flat fees (i.e., per account or per customer fees) representing payment for recordkeeping or administrative services and not for the placement of deposits. The fee arrangements must satisfy Section 23B of the Federal Reserve Act.[37]

(e) Other Issues

Deposit Listing Services. Deposit listing services come in different forms, but all connect those seeking to place a deposit with those seeking a deposit by listing the deposit rates of IDIs. Depositors use listing services to find the best rate available for a given deposit type and, in the case of a CD, a term. Since the statute was first enacted, staff has distinguished between a company that compiles information about interest rates in passive manner versus a deposit broker that is in the business of placing or facilitating the placement of deposits. A particular company can advertise itself as a listing service as well as meet the definition of a “deposit broker.” In recognition of this possibility, staff at the FDIC developed criteria for analyzing whether a “listing service” acts as a “deposit broker.” [38]

In 2004 FDIC staff provided criteria to assist the industry in analyzing whether a deposit listing services would be viewed as a deposit broker. In particular, staff advisory opinions indicate that a listing service is not viewed as a deposit broker if it meets the following criteria:

(1) The person or entity providing the listing service is compensated solely by means of subscription fees (i.e., the fees paid by subscribers as payment for their opportunity to see the rates gathered by the listing service) and/or listing fees (i.e., the fees paid by depository institutions as payment for their opportunity to list or “post” their rates). The listing service does not require a depository institution to pay for other services offered by the listing service or its affiliates as a condition precedent to being listed;

(2) The fees paid by depository institutions are flat fees: They are not calculated on the basis of the number or dollar amount of deposits accepted by the depository institution as a result of the listing or “posting” of the depository institution's rates;

(3) In exchange for these fees, the listing service performs no services except: (A) The gathering and transmission of information concerning the availability of deposits; and/or (B) the transmission of messages between depositors and depository institutions (including purchase orders and trade confirmations). In publishing or displaying information about depository institutions, the listing service must not attempt to steer funds toward particular institutions (except that the listing service may rank institutions according to interest rates and also may exclude institutions that do not pay the listing fee). Similarly, in any communications with depositors or potential depositors, the listing service must not attempt to steer funds toward particular institutions; and

(4) The listing service is not involved in placing deposits. Any funds to be invested in deposit accounts are remitted directly by the depositor to the insured depository institution and not, directly or indirectly, by or through the listing service.[39]

In 2004, when staff last provided its views on listing services, listing services had already evolved into internet exchange platforms with automated order entry and confirmation services. At the time, however, listing service sites did not provide any advice to prospective depositors, and there was only a flat subscription fee paid by both the banks and those seeking to view the posted rates. Today, the FDIC has observed that certain listing service websites provide additional services. For example, based upon information gathered from bankers interested in participating in listing services, the FDIC notes that some listing services appear to:

○ Offer advice to banks on liability and funds management and regulatory compliance screening for subscribing banks.

○ Send customer information (on behalf of the prospective depositors) directly to the banks that are listing rates.

○ Charge a fee to banks based upon the asset size of the bank, rather than a flat subscription fee.

○ Post rates of “featured” or “preferred” vendors at the very top of its rate board.

The FDIC notes the ambiguity over how these new listing service features could be applied in light of the 2004 criteria. The features above seem to indicate that some listing services are no longer acting in a passive capacity but are instead steering deposits to particular institutions or are otherwise providing services that meet the definition of “deposit broker.”

Accounting or related software products that contemplate the bank using the same software. Some companies provide accounting and other administrative support via software services to clients. These companies, on behalf of their clients, place deposits at either one or a group of preferred banks. Because the companies place deposits at IDIs, the software companies meet the definition of “deposit broker” (unless they meet one of the exceptions). The primary purpose exception applies to an agent or nominee whose primary purpose is not the placement of funds with depository institutions. Banks who receive deposits from software companies argue that the primary purpose of the software companies is to provide accounting services (e.g., bankruptcy management) and the placement of deposits is incidental to this purpose. In analyzing whether a particular arrangement meets the primary purpose arrangement, as noted above, staff currently reviews whether the placement (of third party funds) is for a substantial purpose other than to provide (1) deposit insurance, or (2) a deposit-placement service. In previous cases that staff reviewed relating to accounting software products, staff has not distinguished between providing integrated accounting software and providing access to a deposit account that offers core banking functions (such as daily cash management). Moreover, in the previous arrangements that staff has reviewed, there is typically a contractual volume based fee being paid by the bank to the software company based upon the volume of deposits being placed. As a result, staff has viewed that the software companies are incentivized to place funds of prospective depositors at preferred banks because of the fees that the placement generates.

Prepaid cards. Some companies operate general purpose prepaid card programs, in which prepaid cards are sold to members of the public through the assistance of a prepaid card company or a program manager. After collecting funds from the cardholders, sometimes at retail stores or directly from the card company, funds are placed into a custodial deposit account at an insured depository institution (sometimes with “pass-through” deposit insurance coverage). The funds may be accessed by the cardholders through the use of their cards. In regard to this scenario, staff at the FDIC has taken the position that the prepaid card company or the program manager likely qualifies as a “deposit broker” because it is a third party that is in the business of facilitating the placement of customer deposits at an insured depository institution. Some have argued that a particular prepaid card arrangement is covered by the “primary purpose exception”—specifically, that the “primary purpose” of a prepaid card company (in establishing deposit accounts at an insured depository institution) is not to provide the cardholders with a deposit-placement service, but to enable the cardholders to make purchases through the interbank payment system. Staff at the FDIC has not distinguished between (1) acting with the purpose of placing deposits for other parties, and (2) acting with the purpose of enabling other parties to use deposits to make purchases. When funds are placed into demand deposit accounts (as in the case of custodial accounts used by prepaid card companies), the deposits will be available for withdrawals or transfers or spending. Thus, prepaid card companies have not been viewed as meeting the “primary purpose” exception.

Software applications for personal use that involve funds being placed at an insured depository institution. Some applications provide customers the opportunity to link their existing bank accounts (and other accounts, such as credit cards, and 401k)—with software applications—in an effort to provide efficiencies in budgeting, bill-paying, and opening up a new deposit account. In some cases, the application aggregates customer information based upon available account balances and spending patterns and provides that information to depository institutions to assist in targeting certain customers with financial products. Once the customer is targeted with a financial product, the customer may be transferred to the bank to open up the deposit account or the application may assist in transferring customer information to the bank for purposes of establishing the deposit account. The software provider may receive compensation from the financial institution based upon the referral. FDIC staff has received inquiries about whether various arrangements between software applications and IDIs should be viewed as brokered.

D. Interest Rate Restrictions

As noted earlier, the purpose of Section 29 generally is to limit the acceptance or solicitation of certain deposits by insured depository institutions that are not well capitalized. This purpose is promoted through two means: (1) The prohibition against the acceptance of brokered deposits by depository institutions that are less than well capitalized (as described above); and (2) certain restrictions on the interest rates that may be paid by such institutions. In enacting section 29, Congress added the interest rate restrictions to prevent institutions from avoiding the prohibition against the acceptance of brokered deposits by soliciting deposits internally through “money desk operations.” Congress viewed the gathering of deposits by weaker institutions through either third-party brokers or “money desk operations” as potentially an unsafe or unsound practice.[40] The FDIC has simplified the application of these restrictions through two rulemakings.

Under Section 29, well-capitalized institutions can pay any rate of interest on any deposit. However, the statute imposes different interest rate restrictions on different categories of insured depository institutions that are less than well capitalized. These categories are (1) adequately-capitalized institutions with waivers to accept brokered deposits (including reciprocal deposits excluded from being considered brokered deposits); [41] (2) adequately-capitalized institutions without waivers to accept brokered deposits; [42] and (3) undercapitalized institutions.[43] The statutory restrictions for each category are described in detail below.

Adequately-capitalized institutions with waivers to accept brokered deposits. Institutions in this category may not pay a rate of interest on deposits that “significantly exceeds” the following: “(1) The rate paid on deposits of similar maturity in such institution's normal market area for deposits accepted in the institution's normal market area; or (2) the national rate paid on deposits of comparable maturity, as established by the [FDIC], for deposits accepted outside the institution's normal market area.” [44]

Adequately capitalized institutions without waivers to accept brokered deposits. In this category, institutions may not offer rates that “are significantly higher than the prevailing rates of interest on deposits offered by other insured depository institutions in such depository institution's normal market area.” [45] For institutions in this category, the statute restricts interest rates in an indirect manner. Rather than simply setting forth an interest rate restriction for adequately capitalized institutions without waivers, as noted previously, the statute defines the term “deposit broker” to include “any insured depository institution that is not well capitalized . . . which engages, directly or indirectly, in the solicitation of deposits by offering rates of interest which are significantly higher than the prevailing rates of interest on deposits offered by other insured depository institutions in such depository institution's normal market area.” [46] In other words, the depository institution itself is a “deposit broker” if it offers rates significantly higher than the prevailing rates in its own “normal market area.” Without a waiver, the institution cannot accept deposits from a “deposit broker.” Thus, the institution cannot accept these deposits from itself. In this indirect manner, the statute prohibits institutions in this category from offering rates significantly higher than the prevailing rates in the institution's “normal market area.”

Undercapitalized institutions. In this category, institutions may not offer rates “that are significantly higher than the prevailing rates of interest on insured deposits (1) in such institution's normal market areas; or (2) in the market area in which such deposits would otherwise be accepted.” [47]

Rulemakings Related to Section 29's Interest Rate Restrictions

The FDIC has implemented the interest rate restrictions under section 29 of the FDI Act through two rulemakings.[48] Although the statute, as noted above, sets forth a basic framework, it does not provide certain key details, such as definitions for the terms—“national rate,” “significantly exceeds,” “significantly higher,” and “market area.” As a result, in 1992, the FDIC defined these key terms before updating the “national rate” and clarifying the rate restrictions again in 2009.

“Significantly Exceeds.” Through Section 337.6, the FDIC has provided that a rate of interest “significantly exceeds” another rate, or is “significantly higher” than another rate, if the first rate exceeds the second rate by more than 75 basis points.[49] In adopting this standard, the FDIC offered the following explanation: “Based upon the FDIC's experience with the brokered deposit prohibitions to date, it is believed that this number will allow insured depository institutions subject to the interest rate ceilings . . . to compete for funds within markets, and yet constrain their ability to attract funds by paying rates significantly higher than prevailing rates.” [50] This interpretation of the statute has remained unchanged since the 1992 rulemaking.

“Market Area.” In Section 337.6, prior to the adoption of the 2009 final rule, the term “market area” was defined as follows: “A market area is any readily defined geographical area in which the rates offered by an one insured depository institution soliciting deposits in that area may affect the rates offered by other insured depository institutions in the same area.” [51] At the time, the FDIC reasoned that the market area will be determined on a case-by-case basis, based on the evident or likely impact of a depository institution's solicitation of deposits in a particular area, taking into account the means and media used and volume and sources of deposits resulting from such solicitation.[52]

The “National Rate.” In Section 337.6, as part of the 1992 rulemaking, the “national rate” was defined as follows: “(1) 120 percent of the current yield on similar maturity U.S. Treasury obligations; or (2) In the case of any deposit at least half of which is uninsured, 130 percent of such applicable yield.” [53] In defining the “national rate” in this manner, the FDIC understood that the spread between Treasury securities and depository institution deposits can fluctuate substantially over time but relied upon the fact that such a definition is “objective and simple to administer.” [54] By using percentages (120 percent or 130 percent of the yield on U.S. Treasury obligations) instead of a fixed number of basis points, the FDIC hoped to “allow for greater flexibility should the spread to Treasury securities widen in a rising interest rate environment.” In deciding not to rely on published deposit rates, the FDIC offered the following explanation: “The FDIC believes this approach would not be timely because data on market rates must be available on a substantially current basis to achieve the intended purpose of this provision and permit institutions to avoid violations. At this time, the FDIC has determined not to tie the national rate to a private publication. The FDIC has not been able to establish that such published rates sufficiently cover the markets for deposits of different sizes and maturities.” [55]

2009 Rulemaking on the Interest Rate Restrictions

For many years, the 1992 definition of “national rate” functioned well because rates on Treasury obligations tracked closely with rates on deposits. By 2009, however, the rates on certain Treasury obligations were low compared to deposit rates. Consequently, the “national rate” as defined in the FDIC's regulations became artificially low. By setting a low rate, the FDIC's regulations required some insured depository institutions to offer unreasonably low rates on some deposits, thereby restricting access even to market-rate funding.

As part of the 2009 rulemaking, the FDIC addressed two issues that developed after the 1992 rulemaking: (1) The obsolescence of the FDIC's 1992 definition of the “national rate”; and (2) the difficulty experienced by insured depository institutions and examiners in determining prevailing rates in its “market areas.”

In response to the first problem, the FDIC redefined the “national rate” as “a simple average of rates paid by all insured depository institutions and branches for which data are available.” As noted in the 2009 rulemaking, the updated “national rate” methodology represented an objective average and the exclusion of certain branches or offices was viewed by the FDIC, at the time, as contrary to providing a meaningful restriction on insured depository institutions that are not well capitalized.[56]

In response to the second problem, the FDIC created a presumption that the prevailing rate in any market would be the national rate (as defined above). An insured depository institution could rebut this presumption by presenting evidence to the FDIC that the prevailing rate in a particular market is higher than the national rate. If the FDIC agreed with this evidence, the institution would be permitted to pay as much as 75 basis points above the local prevailing rate. In evaluating this evidence, the FDIC may use segmented market rate information (for example, evidence by State, county or MSA). Also, the FDIC may consider evidence as to the rates offered by credit unions but only if the insured depository institution competes directly with the credit unions in the particular market. Finally, the FDIC may consider evidence that the rates on certain deposit products differ from the rates on other products. For example, in a particular market, the rates on NOW accounts might differ from the rates on MMDAs. NOW accounts might be distinguished from MMDAs because the two types of accounts are subject to different legal requirements.[57]

Ultimately, the 2009 rulemaking simplified the approach of applying the rate restrictions and, importantly, has provided community banking institutions, that may not compete in the national deposit marketplace (e.g., listing services), the ability to offer competitive deposit rates in its local market area.

Additional Interest Rate Issues

Since the FDIC's adoption of the 2009 rulemaking, federal funds rates stayed at historically low levels and only recently have begun to rise. In addition, institutions also have created new products that do not fit into the posted national rates and rate caps.

Calculation of rates. Since the crisis that began in 2008, the “national rate” has been relatively low due to the low interest rate environment. Moreover, because the national rate is an average for all banks and branches, the largest banks with large numbers of branches have had a disproportional effect on average interest rates. Even as other interest rates have begun to rise, the average has stayed low as the largest banks have been slow to increase interest rates on deposits.

New products. The FDIC has recently seen an increase in promotional deposit products and products with special features. These products and promotions are generally not compatible with the standard products included in the FDIC's published weekly national rate caps. An example of a product with a special feature is one that provides a one-time cash payment for opening up a deposit account or provides airline miles or other bonuses with specific deposit products. Such deposit products may have common maturities (or be demand accounts) and as a result they may be included as part of the “national rate” calculation without acknowledgement of the up-front payment or other bonus received in place of interest paid on the deposit.

Special features. Some institutions are also offering deposit products with special features that may raise questions about how the rate cap should apply. Below are examples of three types of deposit products with special features:

○ Step up rates. Certain deposit products have variable rate features that allow the interest rate to increase before the deposit matures. With these products, particularly time deposits with longer maturities, the institution could fall to less than well capitalized during the term of the deposit. As a result, and as the FDIC has seen in the past, an institution could pay a rate that exceeds the interest rate restrictions after the downgrade.

○ Atypical maturities. Unusual maturity periods (for example, 13 or 15 months instead of 12 or 18 months) make it difficult to compare with either national rates or prevailing local rates.

○ Exceptionally long maturities for time deposits combined with penalty-free early withdrawal. In some cases, institutions have structured deposit products with exceptionally long maturities in order to extrapolate exceptionally high interest rates for the deposits coupled with withdrawal rights that are significantly shorter than the term of the deposit maturity (e.g., 7 day penalty period on a 5 year certificate of deposit).

III. Request for Comments

The FDIC seeks comment on all aspects of its regulatory approach to brokered deposits and interest rate restrictions, and in particular the following:

○ Are there ways the FDIC can improve its implementation of Section 29 of the FDI Act while continuing to protect the safety and soundness of the banking system? If so, how?

Brokered Deposits

○ Are there types of deposits that are currently considered brokered that should not be considered brokered? If so, please explain why.

○ Are there types of deposits that are currently not considered brokered that should be considered brokered? If so, please explain why.

○ Are there specific changes that have occurred in the financial services industry since the brokered deposits regulation was adopted that the FDIC should be cognizant of as it reviews the regulation? If so, please explain.

○ Do institutions currently have sufficient clarity regarding who is or is not a deposit broker and what is or is not a brokered deposit? Are there ways the FDIC can provide additional clarity through updates to the brokered deposits regulation, consistent with the statute and the policy considerations described above?

○ Are there areas where changes might be warranted but could not be effectuated under the current statute? Are there any statutory changes that warrant consideration from Congress?

○ Should the FDIC make changes to the Call Report instructions so that the agency can gather more granular information about types of brokered deposits?

○ In general, the FDIC welcomes any additional data or market information related to brokered deposits, particularly related to those types of brokered deposits that are not specifically reported by institutions in their Call Reports (e.g., Master Certificates of Deposits held in the name of DTC and deposits placed through unaffiliated sweep programs).

Interest Rate Restrictions

○ Are there alternatives that the FDIC should consider in addressing Section 29's interest rate restrictions for less than well capitalized institutions?

○ Should the methodology used to calculate the “national rate” be changed? If so, how?

○ Should there remain a presumption that the prevailing rate in any “market area” is the national rate? If not, how should the FDIC define the “normal market area”?

○ Should the amount of the rate cap, currently 75 basis points over either the national rate or the prevailing market rate, be revised? If so, how?

○ How should deposits with promotional or special features be treated with respect to the national rate or the prevailing market rate?

○ How should the rates offered by internet-based or electronic commerce-based institutions be calculated?

Appendix 1

Descriptive Statistics on Core and Brokered Deposits

Core Deposits

Core deposits are not defined by statute. Rather, they are defined for analytical and examination purposes in the Uniform Bank Performance Report (UBPR). Through 2010, the Federal Financial Institutions Examination Council (FFIEC) defined “core deposits” to include all demand and savings deposits, including money market deposit, NOW and ATS accounts, other savings deposits, and time deposits in amounts under $100,000.[58] Under this definition, core deposits were equivalent to total domestic deposits less time deposits over $100,000 and included insured brokered deposits. As of March 31, 2011, the definition was revised to reflect the permanent increase to FDIC deposit insurance coverage from $100,000 to $250,000 and to exclude insured brokered deposits from core deposits. This revision defines core deposits as the sum of demand deposits, all NOW and ATS accounts, MMDAs, other savings deposits and time deposits under $250,000, minus all brokered deposits under $250,000. For periods before March 2011, the definition was revised to the sum of demand deposits, all NOW and ATS accounts, MMDAs, other savings deposits and time deposits under $100,000, minus all brokered deposits under $100,000.

Historically, reliance on core deposits has varied by bank size. Banks with less than $1 billion in total assets generally have had the heaviest reliance on core deposits, and banks with $50 billion or more in total assets have had the least reliance on core deposits. Since 2010, the ratio of core deposits to total assets has changed less for smaller banks than it has for larger banks. At year-end 2010, core deposits equaled 75 percent of total assets at banks with less than $1 billion in assets, but only 47 percent for banks with $50 billion or more in total assets. By the third quarter of 2018, core deposits equaled 76 percent of total assets at banks with less than $1 billion in assets and 58 percent of at banks with $50 billion or more in total assets (See Chart 1.)

Through mid-year 2009, almost all core deposits at community banks were estimated to be insured, but, at the end of third quarter 2009, when banks began reporting insured deposits at the then temporary insurance limit of $250,000, estimated insured deposits were greater than core deposits. Estimated insured deposits represented a smaller share of core deposits at the largest banks, as a result of their holdings of large uninsured demand deposits. At September 30, 2010, for banks with assets over $50 billion, estimated insured deposits represented only 69 percent of core deposits, but, at March 31, 2011, after the coverage of all noninterest bearing transaction accounts over $250,000 was established temporarily under the Dodd-Frank Act, estimated insured deposits rose to 84 percent. (See Chart 2.)

Note:

From October 14, 2008 to December 31, 2010, domestic non-interest bearing transaction accounts were guaranteed in full under the Transaction Account Guarantee Program (TAG), part of the FDIC's Temporary Liquidity Guarantee Program (TLGP). From December 31, 2010 to December 31, 2012, the Dodd-Frank Act provided temporary unlimited deposit insurance coverage for non-interest bearing transaction accounts. These programs account for the observed shifts up and down in the Estimated Insured Deposits as a Share of “Core” Deposits shown in the chart during these periods.

Effective with the March 31, 2011, UBPR, the FFIEC revised the definition of core deposits to take into account the increase in the deposit insurance limit to $250,000 under Dodd-Frank. The new definition includes time deposits up to $250,000 but excludes brokered deposits of any denomination. Using Call Report and Thrift Financial Report (TFR) data as of March 31, 2011, the new definition of core deposits added $24.9 billion (or 0.3 percent) to core deposits. However, the increase in core deposits, as the result of the new definition, occurred almost exclusively at smaller banks and thrifts, since the decrease in core deposits due to exclusion of brokered deposits tended to be less than the increase in core deposits due to inclusion of time deposits within the new threshold of up to $250,000. Core deposits at banks and thrifts with assets under $10 billion increased by $143.2 billion under the new definition, but core deposits at banks with assets of at least $10 billion declined by $118.3 billion. Large credit card banks and specialty lenders with affiliated brokerage firms were among those banks with the largest decline in core deposits as a result of the revised definition.

Brokered Deposits

FDIC-insured banks report total brokered deposits and the amount of brokered deposits under the insurance limit on their Call Reports and TFRs. Before 2010, brokered deposits were reported as insured, as any deposits, up to the $100,000 threshold. Beginning March 31, 2010, the threshold for reporting insured brokered deposits on Call Reports and TFRs was increased to $250,000.[61] Insured depository institutions also began reporting total reciprocal brokered deposits in their June 30, 2009, Call Reports and TFRs. The Economic Growth, Regulatory Reform, and Consumer Protection Act, enacted on May 24, 2018, allows certain banks to except a limited amount of reciprocal deposits from brokered deposits.

As of September 30, 2018, brokered deposits totaled $985.7 billion. Fewer than half of all FDIC-insured banks (2,221 banks, or 40.6 percent) reported brokered deposits on their September 30, 2018, Call Reports. As of this date, brokered deposits made up 8.0 percent of industry domestic deposits, in contrast to second quarter 2009 when banks began reporting total reciprocal brokered deposits, brokered deposits accounted for 10.1 percent of industry domestic deposits.

| Asset size group | Total number of banks | Number of banks with brokered deposits | Total brokered deposits (billions) | Share of total brokered deposits (%) | Total domestic deposits | Share of total domestic deposits (%) |

|---|---|---|---|---|---|---|

| Under $1 Billion | 4,704 | 1,656 | $31.92 | 3.2 | $988.05 | 8.0 |

| $1-10 Billion | 635 | 439 | 90.16 | 9.1 | 1,349.56 | 11.0 |

| $10-50 Billion | 97 | 89 | 171.87 | 17.4 | 1,605.40 | 13.0 |

| Over $50 Billion | 41 | 37 | 691.78 | 70.2 | 8,378.84 | 68.0 |

| All Banks | 5,477 | 2,221 | 985.73 | 12,321.84 |

Brokered deposits typically make up a lower share of deposit funding for small banks compared to banks with $10 billion or more in assets. In aggregate, banks with assets between $10 billion and $50 billion reported brokered deposits equal to 10.7 percent of their domestic deposits as of September 30, 2018, the highest of any asset cohort group, while banks with assets under $1 billion reported brokered deposits equal to just 3.2 percent of domestic deposits. (See Chart 3.)

Note:

The reversal of growth in the use of brokered deposits occurring between 2009 and 2012 is likely the joint result of the dramatic decline in interest rates occurring over that period, coupled with significant new restrictions on the use of brokered deposits by banks classified as adequately and undercapitalized.

At the end of the third quarter of 2018, insured brokered deposits made up more than 82.5 percent of total brokered deposits at all banks. Insured brokered deposits as a percent of all brokered deposits was highest at banks with assets of $50 billion or less. In aggregate, insured brokered deposits made up 93.7 percent of total brokered deposits at banks with assets between $1-10 billion, as compared to 79.5 percent at banks with assets greater than $50 billion. (See Chart 4.)

Section 29 of the Federal Deposit Insurance Act (FDI Act) sets forth restrictions on the acceptance of brokered deposits that also appear in the FDIC's regulations.[62] Under Section 29, banks are restricted from accepting, renewing, or rolling over brokered deposits if they are less than well capitalized. This restriction may be waived for adequately capitalized banks. Undercapitalized institutions are not allowed to receive new brokered deposits and must follow an FDIC-approved plan to remove them from their books over time. After rising to a peak in mid-2009, the use of brokered deposits as a share of domestic deposits declined for both adequately capitalized banks and well capitalized banks. As of September 30, 2018, of the 5,477 insured depository institutions, 99.6 percent were well capitalized, while 0.2 percent were rated as adequately capitalized. Of those rated as adequately capitalized, roughly half held brokered deposits. (See Chart 5.) [63]

Brokered Deposits during the 2007-2017 Financial Crisis

During the financial crisis and the years that followed, from the beginning of 2007 through the end of 2017, the Deposit Insurance Fund (DIF) incurred $74.4 billion in losses as of December 31, 2016. During this period, excluding Washington Mutual, 530 banks failed and were placed in FDIC receivership.

Typically, as institutions get closer to failure, their capital level declines and they are no longer able to accept, renew, or roll over brokered deposits, so levels of brokered deposits at failure are usually low. Nevertheless, of the 530 failed banks, twelve, approximately 2.3 percent, held a majority (50% or greater) as brokered deposits; 280 or approximately 52.8 percent, held less than 1% of their total deposits as brokered deposits.[64] (See Chart 6.)

| Brokered deposits as % of total deposits | Number failed institutions w/DTC-titled brokered CDs | % of Institutions | Number failed institutions w/non-DTC titled brokered deposits 65 | % of institutions | Number failed institutions w/internet deposits |

|---|---|---|---|---|---|